Updated: 16 May 2026

Indian investors are becoming cautious again.

After months of market volatility in 2026, many families are shifting part of their money toward fixed deposits for stability and predictable returns. At the same time, Small Finance Banks are attracting attention because some of them are offering FD rates above 8%.

That naturally creates an important question:

Are Small Finance Bank FDs actually safe?

Many investors now compare:

- SFB FD rates

- SBI FD safety

- HDFC and ICICI fixed deposits

- DICGC insurance protection

- emergency fund safety

The confusion is understandable.

Higher FD rates look attractive, especially for:

- retirees

- senior citizens

- conservative savers

- middle-class families protecting emergency money

But safety matters more than interest rate alone.

This guide explains:

- how safe Small Finance Bank FDs are in 2026

- how DICGC insurance works

- differences between SFBs and large banks

- real risks investors should understand

- practical FD diversification strategies for Indian households

Disclaimer: FD rates, bank policies, and regulations may change. Verify latest details from official bank websites, RBI, and DICGC before investing. Educational content only.

Why Are Small Finance Bank FD Rates Higher?

This is the first thing most investors notice.

Some Small Finance Banks are offering FD rates above:

- 8%

- 8.25%

- even 8.5% on selected tenures

Meanwhile, large banks like:

- SBI

- HDFC Bank

- ICICI Bank

usually remain closer to:

- 6.5% to 7.25%

depending on tenure and customer category.

That difference attracts depositors quickly.

But higher FD rates do NOT automatically mean a bank is unsafe.

Small Finance Banks are still expanding aggressively and need to attract deposits faster than large established banks. Offering higher interest rates is one way to grow their deposit base.

Large banks already have:

- massive customer networks

- stronger liquidity

- larger deposit pools

- stronger public trust

So they do not need to compete aggressively on FD rates.

What Is a Small Finance Bank?

Small Finance Banks are RBI-regulated banks created to improve banking access in underserved segments of India.

They can:

- accept deposits

- offer fixed deposits

- provide savings accounts

- issue debit cards

- provide loans

- offer digital banking services

Examples include:

- AU Small Finance Bank

- Unity Small Finance Bank

- Suryoday Small Finance Bank

- ESAF Small Finance Bank

- Ujjivan Small Finance Bank

One important point:

Small Finance Banks are regulated banks, not unregulated deposit schemes or finance companies.

They operate under RBI banking regulations and must follow rules related to:

- capital adequacy

- liquidity management

- CRR and SLR requirements

- prudential norms

- priority sector lending obligations

This regulatory framework is one reason SFB deposits remain part of India’s formal banking system.

Are Small Finance Bank FDs Covered by DICGC?

Yes.

This is one of the most important facts investors should understand before comparing FD safety.

Deposits in eligible Small Finance Banks are covered under:

DICGC insurance

DICGC stands for:

Deposit Insurance and Credit Guarantee Corporation

It operates under the RBI framework.

What Does the ₹5 Lakh DICGC Cover Mean?

Many depositors misunderstand this rule.

The insurance limit is:

₹5 lakh per depositor per bank

And this includes:

- principal

- accumulated interest

together.

Example:

If you have:

- ₹4.8 lakh FD

- ₹35,000 interest

Total deposit value becomes:

₹5.15 lakh

In this case, DICGC protection applies up to ₹5 lakh.

Important DICGC Rule Most Investors Miss

DICGC coverage applies:

per depositor per bank

NOT:

- per FD

- per account

- per branch

This means:

If a person keeps:

- ₹10 lakh

- ₹15 lakh

- ₹20 lakh

inside one single bank,

the amount above ₹5 lakh remains outside insurance coverage.

This applies to:

- Small Finance Banks

- SBI

- HDFC Bank

- ICICI Bank

- most insured banks in India

Are SFB FDs as Safe as SBI or HDFC FDs?

This question needs a balanced answer.

Technically:

- both are RBI regulated

- both are covered under DICGC insurance

- both operate inside India’s banking framework

But practically, many investors still perceive differences.

Large banks like:

- SBI

- HDFC Bank

- ICICI Bank

usually have:

- larger balance sheets

- wider branch networks

- stronger public trust

- larger customer bases

- longer operating history

Small Finance Banks are smaller institutions and often focus more heavily on:

- retail lending

- small borrowers

- MSMEs

- underserved sectors

That does NOT automatically make them unsafe.

But because they are smaller institutions, deposit concentration and liquidity planning become more important for households parking large sums.

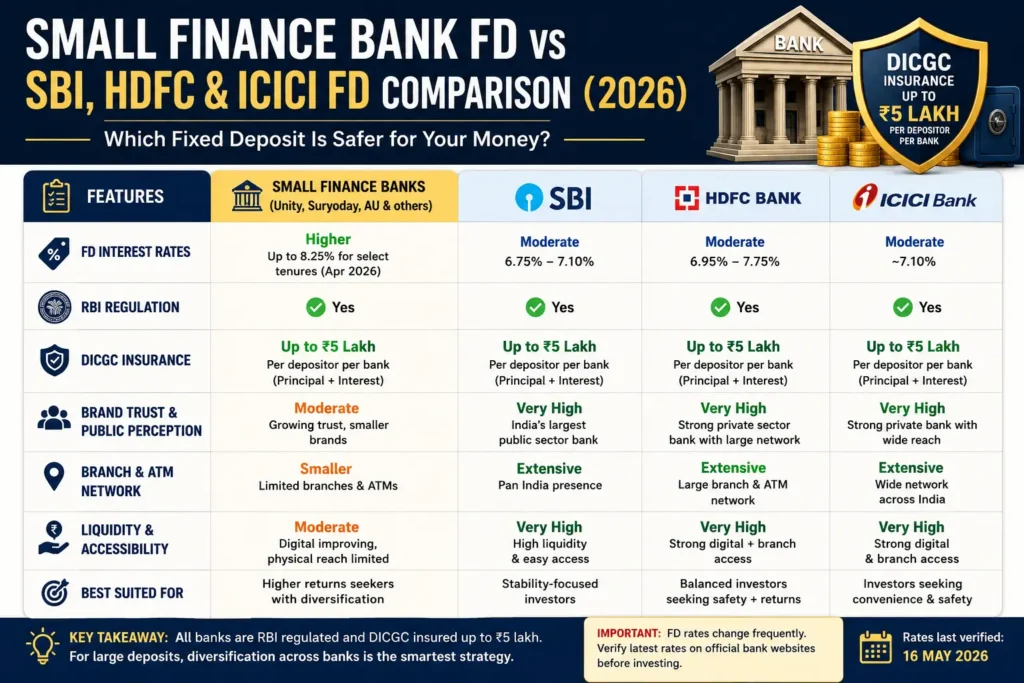

SFB FD vs SBI, HDFC & ICICI FD Comparison (2026)

| Feature | Small Finance Banks | SBI / HDFC / ICICI |

|---|---|---|

| FD Rates | Usually higher | Usually lower |

| RBI Regulation | Yes | Yes |

| DICGC Protection | Up to ₹5 lakh | Up to ₹5 lakh |

| Public Trust | Moderate to growing | Very strong |

| Branch Network | Smaller | Extensive |

| Liquidity Comfort | Moderate | Higher |

| Emergency Fund Suitability | Partial allocation | Strong |

| Best For | Higher-rate seekers with diversification | Stability-focused savers |

FD Rates Snapshot (Last Verified: 16 May 2026)

| Bank | Approx FD Rate |

|---|---|

| Suryoday SFB | Up to 8.25% |

| Unity SFB | Around 8.00% |

| AU SFB | Around 7.5%+ |

| SBI | Around 6.75%–7.10% |

| HDFC Bank | Around 6.95%–7.75% |

| ICICI Bank | Around 7.10% |

Rates vary based on tenure, customer category, and bank policy. Always verify latest official rate cards before investing.

Why SFBs Can Offer Higher Rates

Small Finance Banks were designed to serve:

- underserved borrowers

- small businesses

- rural and semi-urban customers

- microfinance segments

Because they are still expanding their deposit base, they often compete more aggressively for retail deposits.

That is one reason many SFBs offer higher FD returns than large banks.

Higher rates usually reflect:

- growth strategy

- deposit acquisition needs

- smaller scale operations

not automatic financial weakness.

What Are the Real Risks of SFB FDs?

The discussion should not become:

- “safe”

or - “unsafe”

The better approach is understanding practical risks.

1. Deposit Concentration Risk

Keeping very large amounts in one bank increases exposure.

Especially for:

- retirees

- emergency reserves

- senior citizen lifetime savings

Diversification matters more than chasing every extra 0.5% return.

2. Liquidity and Accessibility

Large banks usually offer:

- wider branch access

- larger ATM networks

- stronger operational familiarity

Some investors value that convenience and comfort.

3. Business Concentration Risk

Many SFBs lend more aggressively toward:

- MSMEs

- microfinance

- small borrowers

Economic slowdowns can affect these segments more heavily.

4. Emotional Comfort

This matters more than people admit.

Some investors simply feel calmer keeping emergency money in:

- SBI

- HDFC Bank

- ICICI Bank

That emotional comfort has real value in financial planning.

Who Should Consider Small Finance Bank FDs?

SFB FDs may suit:

- investors seeking higher FD rates

- diversified savers

- limited higher-yield allocations

- short-to-medium-term FD investors

They may work especially well when:

- deposits remain within planned limits

- money is diversified across banks

- emergency liquidity exists elsewhere

Who Should Be More Careful?

Extra caution may make sense for:

- retirees putting entire savings into one SFB

- households with weak emergency reserves

- investors crossing DICGC limits heavily

- families fully dependent on FD income

For such households:

- stability

- diversification

- liquidity

matter more than maximizing yield.

Smart FD Diversification Strategy

Instead of chasing only the highest FD rate, many households may benefit more from:

diversified FD planning

Example:

| Purpose | Suggested Placement |

|---|---|

| Emergency liquidity | SBI/HDFC savings + sweep FD |

| Core stable reserve | Large bank FD |

| Higher-yield allocation | Limited SFB FD exposure |

| Long-term allocation | Diversified mix across banks |

This approach reduces:

- concentration risk

- liquidity pressure

- panic during uncertainty

FD Laddering Strategy Example

Instead of locking all money into one FD:

Split deposits across:

- 1 year

- 2 years

- 3 years

- 5 years

This creates:

- periodic liquidity

- reinvestment flexibility

- better interest-rate adaptability

Especially useful during changing rate cycles.

Should Senior Citizens Use SFB FDs?

Some senior citizens do use them because:

- rates are attractive

- income needs are higher

- post-retirement returns matter

But retirees should usually avoid:

- putting entire retirement corpus into one bank

- chasing only highest rates

- ignoring DICGC limits

Balanced diversification is usually safer.

Biggest FD Mistakes Investors Make

Chasing Only Highest Rate

Higher return without diversification creates unnecessary exposure.

Ignoring DICGC Limits

Very common mistake.

Many depositors incorrectly assume insurance applies separately for every FD.

Locking Emergency Money for Long Tenures

Emergency liquidity should remain accessible.

Keeping Entire Savings in One Bank

Diversification reduces stress and concentration risk.

Practical Rule for Indian Families

For many households:

- stability

- liquidity

- emergency reserves

- diversification

matter more than maximizing every extra 0.5% FD return.

That mindset usually creates stronger long-term financial stability.

FAQs

Are Small Finance Bank FDs safe in India?

SFB FDs are RBI regulated and covered under DICGC insurance up to ₹5 lakh per depositor per bank.

What happens if a Small Finance Bank fails?

Eligible deposits remain protected under DICGC rules up to applicable insurance limits.

Is DICGC protection automatic?

Yes. Eligible insured bank deposits are automatically covered.

Does DICGC cover both principal and interest?

Yes. Total coverage includes both principal and accumulated interest together.

Is ₹10 lakh safe in one Small Finance Bank?

Only ₹5 lakh per depositor per bank falls under DICGC insurance coverage.

Are SBI FDs safer than SFB FDs?

Large banks generally have stronger public trust and larger balance sheets, although both operate under RBI regulation.

Why do Small Finance Banks offer higher FD rates?

Many SFBs offer higher rates to attract deposits and expand their customer base.

Should senior citizens invest in SFB FDs?

Some may choose limited exposure, but diversification is usually important for retirement savings.

Are FD returns guaranteed?

FD rates are fixed for the chosen tenure at the time of deposit, subject to bank terms and applicable conditions.

What is the safest FD strategy?

Diversification across banks, maintaining liquidity, and understanding DICGC limits generally improve safety.

Conclusion

Small Finance Bank FDs are not automatically unsafe.

They are:

- RBI regulated

- part of India’s banking framework

- covered under DICGC insurance limits

But investors should still understand:

- deposit concentration risk

- liquidity planning

- diversification

- insurance limits

For many Indian households, the smarter strategy is not:

- blindly chasing highest FD rates

or - avoiding SFBs completely

The better approach is balanced financial planning.

That means:

- diversifying deposits

- maintaining emergency liquidity

- understanding DICGC protection

- matching FD strategy with household needs

Higher returns matter.

But financial stability matters more.

Suggested Internal Links

- SIP During Market Fall in India

- Emergency Fund Guide

- PPF vs FD 2026

- Best Low-Risk Investments India

- FD Laddering Strategy

- Senior Citizen Investment Options

Suggested CTA

Download:

“2026 FD Safety & Emergency Money Checklist for Indian Families”

Includes:

- DICGC safety checklist

- FD diversification tracker

- emergency reserve planner

- FD laddering worksheet