Buying a home is the biggest financial decision most Indians make. A small difference in interest rate can save or cost you lakhs over 20 years. This guide covers everything, current rates, eligibility, PMAY subsidy, tax benefits and how to choose the right lender.

This guide uses verified data from RBI, NHB, Paisabazaar and official sources as of April 2026.

Indian Housing Market – April 2026

| Metric | Data |

|---|---|

| H1 FY2025-26 home loans disbursed | Rs.4,31,725 crore |

| Loans above Rs.25 lakh share | 60.85% of disbursements |

| Loans with tenure above 7 years | 97.52% |

| Cities with price appreciation | 46 out of 50 cities |

| Gurugram price increase (highest) | 25.9% annual |

| Bengaluru price increase | 11.3% annual |

| NHB HPI composite increase | 4.8-5.0% Y-o-Y |

India’s housing market remains strong. Property prices rising in 46 of 50 cities shows sustained demand across the country.

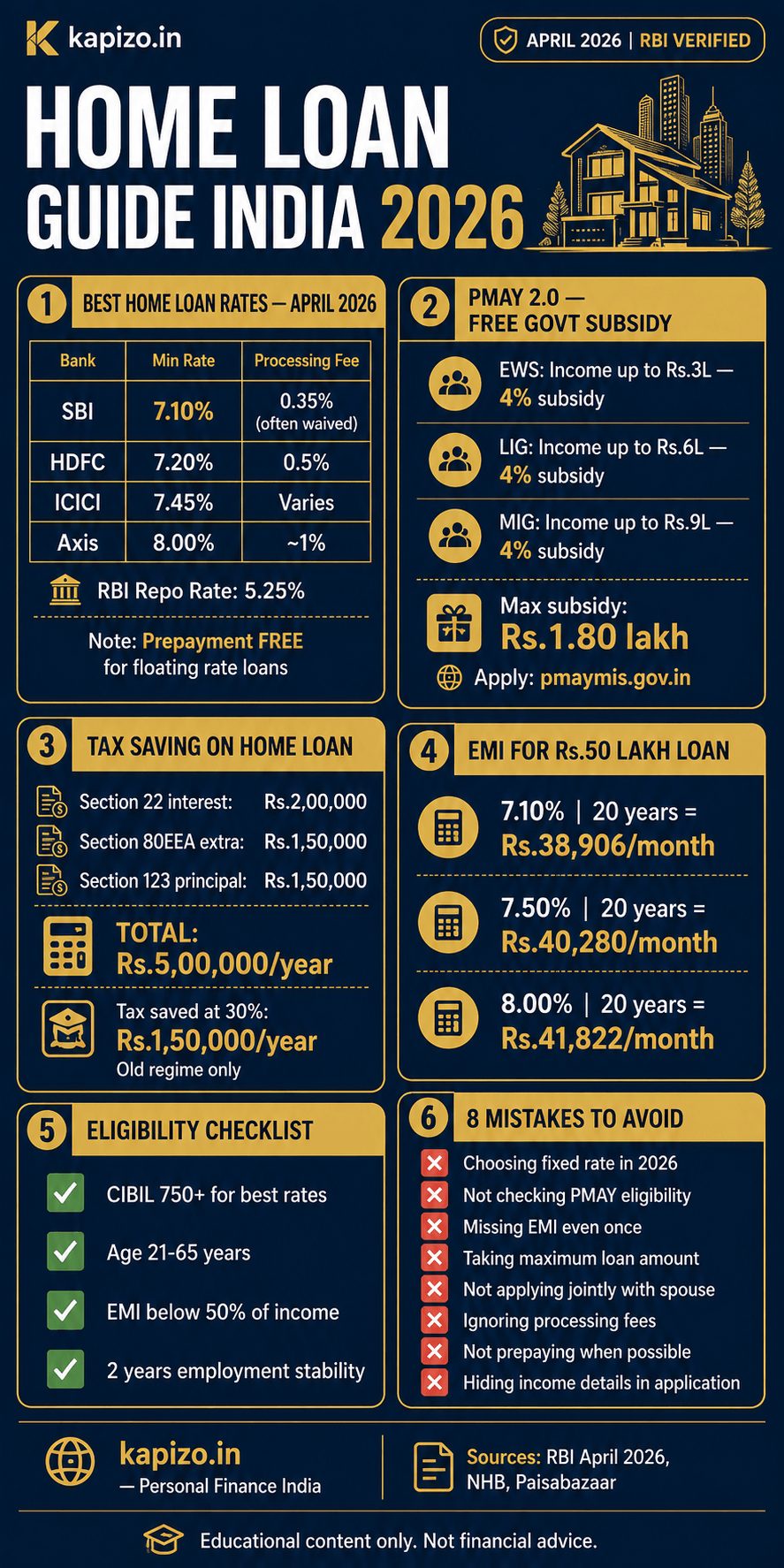

Current Home Loan Interest Rates – April 2026

RBI Repo Rate: 5.25% (after 125 bps cumulative cut in 2025)

| Bank | Min Rate | Max Rate | Processing Fee |

|---|---|---|---|

| SBI | 7.10% | ~7.50% | Up to 0.35%, max Rs.12,000 (often waived) |

| HDFC Bank | 7.20% | ~8.40% | 0.5% or Rs.4,000+ |

| ICICI Bank | 7.45% | ~8.75% | Varies by profile |

| Axis Bank | 8.00% | 8.85% | ~1% min Rs.10,000 + GST |

Source: RBI April 2026, Paisabazaar, BankBazaar, Urban Money. Rates vary by CIBIL score, loan amount, employment type and promotional offers. Always verify current rates from official bank websites before applying.

Floating vs Fixed Rate

| Factor | Floating Rate | Fixed Rate |

|---|---|---|

| Starting rate | 7.10% onwards | 9.5%+ p.a. |

| Linked to | RBI repo rate (EBLR/RLLR) | Not linked |

| EMI stability | Changes with repo rate | Stable throughout |

| Prepayment charges | FREE (RBI rule Jan 2026) | 0.5-2% penalty |

| Best for | Most borrowers | Those wanting certainty |

Floating rate is best for most Indians in 2026. RBI already cut repo rate by 125 bps in 2025. Further cuts are possible. Floating rate borrowers benefit automatically when rates fall.

Important: Under RBI rules effective January 2026, prepayment is completely free for floating rate home loans. No penalty whatsoever.

Home Loan Eligibility

CIBIL Score

- Minimum: 700+

- Best rates at: 750+

- Below 650: Difficult approval + higher rate

Age

- Minimum: 21 years

- Maximum: 60-65 years at loan maturity (salaried)

- Self-employed: Up to 70 years at maturity

FOIR Rule

Total EMIs including new home loan should not exceed 50% of monthly income.

Employment

- Salaried: Minimum 2 years total experience, 6 months current employer

- Self-employed: Minimum 3 years business stability

Documents Required

Salaried Employees

- PAN card + Aadhaar card

- Last 3 months salary slips

- Last 6 months bank statements

- Form 16 or last 2 years ITR

- Employment letter

- Property documents (agreement, approved plan)

Self-Employed

- PAN card + Aadhaar card

- Last 2-3 years ITR with computation

- Last 12 months bank statements

- Business proof (GST, shop act, partnership deed)

- Property documents

PMAY 2.0 – Government Housing Subsidy 2026

PMAY 2.0 Urban is fully active, launched September 17, 2024.

| Category | Annual Income | Subsidy |

|---|---|---|

| EWS | Up to Rs.3 lakh | 4% on first Rs.8 lakh |

| LIG | Up to Rs.6 lakh | 4% on first Rs.8 lakh |

| MIG | Up to Rs.9 lakh | 4% on first Rs.8 lakh |

Maximum interest subsidy: Rs.1.80 lakh

Conditions:

- Loan value up to Rs.25 lakh

- Property value up to Rs.35 lakh

- Tenure up to 12 years for subsidy calculation

PMAY Progress as of November 2025:

- PMAY-G Rural: 2,90,25,443 houses completed

- PMAY-U Urban: 96.06 lakh houses completed

- PMAY-U 2.0 subsidy: Released to 10,439 beneficiaries

How to Apply:

- Visit pmaymis.gov.in

- Click Citizen Assessment

- Select your category (EWS/LIG/MIG)

- Submit Aadhaar + self-certificate of income

- Apply through empanelled bank or HFC

Home Loan Tax Benefits – FY 2026-27

Old regime only. New regime = no home loan deductions.

| Section | What | Limit |

|---|---|---|

| Section 22 / 24(b) | Home loan interest | Rs.2,00,000/year |

| Section 123 / 80C | Principal repayment | Within Rs.1,50,000 limit |

| Section 80EEA | First-time buyer extra interest | Additional Rs.1,50,000 |

Maximum deduction for first-time buyer:

Section 22 interest: Rs.2,00,000

Section 80EEA extra: Rs.1,50,000

Section 123 principal: Rs.1,50,000

Total: Rs.5,00,000 per year

Tax saved at 30% slab = Rs.1,50,000 per year

Budget 2026 change: Deemed rent tax on second homes removed. If you own two properties, second property no longer taxed on deemed rental income even if vacant.

EMI Reference – Rs.50 Lakh Home Loan

| Rate | 15 years | 20 years | 25 years |

|---|---|---|---|

| 7.10% | Rs.45,392 | Rs.38,906 | Rs.35,322 |

| 7.50% | Rs.46,373 | Rs.40,280 | Rs.36,754 |

| 8.00% | Rs.47,783 | Rs.41,822 | Rs.38,591 |

| 8.85% | Rs.50,117 | Rs.44,350 | Rs.41,313 |

Use our free EMI Calculator at kapizo.in/tools/emi-calculator/

Home Loan vs Renting

| Factor | Home Loan | Renting |

|---|---|---|

| Monthly outflow | Higher EMI | Lower rent |

| Asset creation | Yes, own property | No |

| Flexibility | Low, locked in | High, can move |

| Tax benefit | Up to Rs.5L/year | HRA benefit |

| Long term 10+ years | Better financially | Loses to ownership |

| Short term under 3 years | Not recommended | Better option |

Simple rule:

- Planning to stay 5+ years in same city = buy

- May relocate within 3 years = rent

- EMI less than 40% of income = consider buying

- Property prices rising fast in your city = buy sooner

How to Get Lowest Home Loan Rate

- Maintain CIBIL score above 750

- Check pre-approved offers on your bank app first

- Compare minimum 3-4 lenders before deciding

- Choose floating rate over fixed in 2026

- Opt for shorter tenure if budget allows

- Negotiate processing fee waiver

- Check PMAY eligibility before applying

- Apply jointly with spouse for higher eligibility

Step by Step Home Loan Process

- Check CIBIL score free on Paisabazaar or BankBazaar

- Calculate budget, max EMI = 40% of income

- Use EMI calculator at kapizo.in/tools/emi-calculator/

- Check PMAY eligibility at pmaymis.gov.in

- Compare rates on Paisabazaar or BankBazaar

- Check pre-approved offers on your existing bank app

- Submit application with all documents

- Property valuation by bank

- Legal verification of property documents

- Loan sanction letter issued

- Disbursement on property registration

Common Home Loan Mistakes to Avoid

- Taking maximum possible loan (strains finances for 20 years)

- Choosing fixed rate in 2026 (floating is better now)

- Not checking PMAY eligibility (free Rs.1.80 lakh subsidy missed)

- Ignoring processing fees in lender comparison

- Not making part prepayment when extra funds available

- Missing EMI even once (CIBIL drops sharply)

- Not taking joint loan with spouse (loses double tax benefit)

- Buying overpriced property just because loan is approved

Frequently Asked Questions

Q: What is the current lowest home loan rate in India?

SBI offers lowest starting rate at 7.10% p.a. as of April 2026, linked to RBI repo rate of 5.25%. Actual rate depends on CIBIL score, income, and loan amount.

Q: How much home loan can I get on Rs.50,000 salary?

At 40-50% FOIR, EMI eligibility is Rs.20,000-25,000 per month. At 7.50% for 20 years, this translates to approximately Rs.24-30 lakh loan eligibility. Higher CIBIL and spouse income increases this.

Q: Is PMAY subsidy still available in 2026?

Yes. PMAY 2.0 Urban is fully active. Families with income up to Rs.9 lakh are eligible for 4% interest subsidy on first Rs.8 lakh of loan, saving maximum Rs.1.80 lakh. Apply at pmaymis.gov.in.

Q: Can I claim both HRA and home loan tax benefit?

Yes. If you own property in one city but live on rent in another city for work, you can claim both HRA exemption and home loan deductions simultaneously.

Q: Should I prepay home loan or invest in mutual funds?

If home loan rate is 7.5% and mutual fund SIP returns 12%+ historically, investing is better mathematically. But prepayment gives guaranteed savings. Ideal approach is to do both.

Q: What is EBLR and how does it affect my home loan?

EBLR is External Benchmark Lending Rate, linked directly to RBI repo rate. When RBI cuts repo rate, your home loan rate drops automatically within 3 months. RBI cut 125 bps in 2025, benefiting existing floating rate borrowers.

Q: Is second home loan interest deductible?

Yes. For let-out property, full interest is deductible with no Rs.2 lakh cap. For second self-occupied property, Rs.2 lakh cap applies. Budget 2026 removed deemed rent tax on second homes.Disclaimer: Interest rates and eligibility criteria change frequently. PMAY scheme terms subject to government updates. Data sourced from RBI April 2026, NHB Housing Finance Report, Paisabazaar, BankBazaar, Urban Money, verified April 2026. Always verify from official bank websites and pmaymis.gov.in. Kapizo.in may earn affiliate commission from links on this page. Not financial advice.