India’s tax system changed completely from April 1, 2026. The old Income Tax Act 1961 is replaced by the Income-tax Act, 2025 (ITA 2025). New slabs, new section numbers, higher allowances — this guide covers everything salaried Indians need to know for FY 2026-27.

Source: Income-tax Act 2025, Finance Bill 2026, Income Tax Rules 2026, verified via official government documents from finmin.nic.in and incometax.gov.in

What Changed — ITA 2025 vs Old Act 1961

| Feature | Old ITA 1961 | New ITA 2025 |

|---|---|---|

| Effective from | 1961 | April 1, 2026 |

| Assessment Year | Separate concept | Replaced by “Tax Year” |

| Section 80C | Section 80C | Section 123 |

| Home loan interest | Section 24(b) | Section 22 |

| NPS deduction | Section 80CCD(1B) | Section 124(3) |

| Language | Complex legal | Simplified |

| PAN | Continues unchanged | Continues unchanged |

Important: All existing rights, pending proceedings, and PAN cards remain valid. Only the law’s language and structure changed — not your obligations.

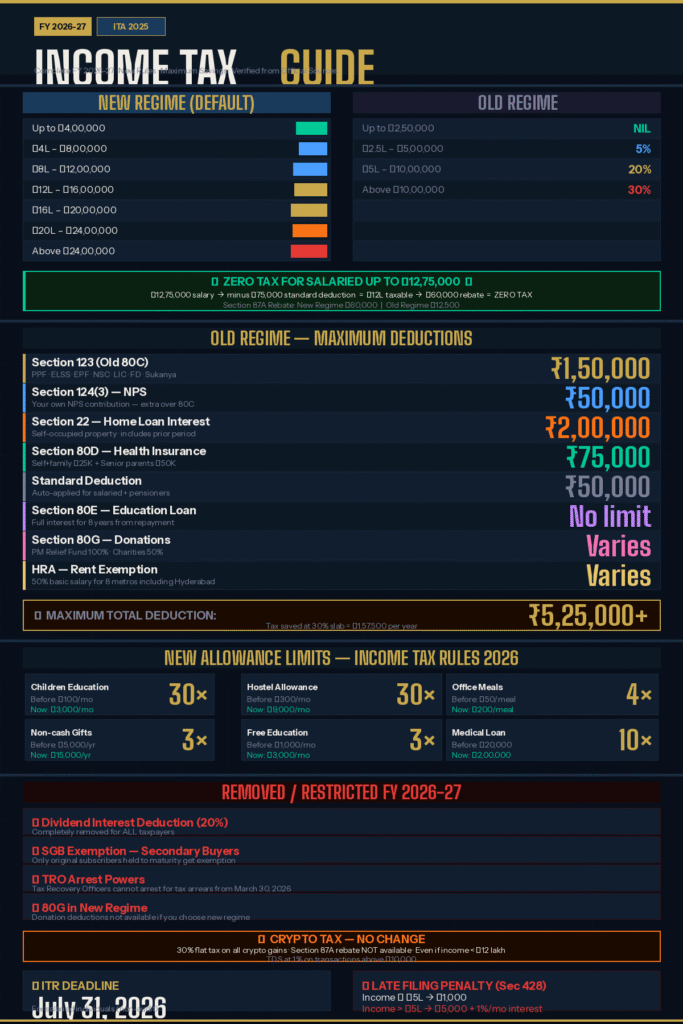

Income Tax Slabs FY 2026-27

New Tax Regime — Default (ITA 2025 Section 202)

| Income Range | Tax Rate |

|---|---|

| Up to ₹4,00,000 | Nil |

| ₹4,00,001 – ₹8,00,000 | 5% |

| ₹8,00,001 – ₹12,00,000 | 10% |

| ₹12,00,001 – ₹16,00,000 | 15% |

| ₹16,00,001 – ₹20,00,000 | 20% |

| ₹20,00,001 – ₹24,00,000 | 25% |

| Above ₹24,00,000 | 30% |

Plus 4% Health and Education Cess on tax amount.

Surcharge (New Regime):

- Income ₹50L – ₹1Cr: 5%

- Income ₹1Cr – ₹2Cr: 15%

- Income above ₹2Cr: 25%

Note: The 37% surcharge rate applies only to old regime. New regime maximum surcharge = 25%.

Old Tax Regime (Must actively select)

| Income Range | Tax Rate |

|---|---|

| Up to ₹2,50,000 | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% |

| ₹5,00,001 – ₹10,00,000 | 20% |

| Above ₹10,00,000 | 30% |

Section 87A Rebate — Zero Tax Explained

| Feature | New Regime | Old Regime |

|---|---|---|

| Zero tax up to | ₹12,00,000 | ₹5,00,000 |

| Maximum rebate | ₹60,000 | ₹12,500 |

| Standard deduction | ₹75,000 | ₹50,000 |

| Effective zero-tax salary | ₹12,75,000 | ₹5,50,000 |

How it works (New Regime example):

- Gross salary: ₹12,75,000

- Minus standard deduction: ₹75,000

- Taxable income: ₹12,00,000

- Tax on slabs: ₹60,000

- Minus 87A rebate: ₹60,000

- Final tax payable: ZERO

Important: Section 87A rebate does NOT apply to special rate income like crypto gains, capital gains, or online gaming winnings — even if total income is below ₹12 lakh.

New Regime — What’s Available

| Deduction | Limit | Available? |

|---|---|---|

| Standard Deduction (salaried + pensioners) | ₹75,000 | ✅ Yes |

| Section 87A Rebate | ₹60,000 | ✅ Yes |

| Employer NPS Contribution | No limit | ✅ Yes |

| Section 123 (80C investments) | ₹1,50,000 | ❌ No |

| HRA | Depends | ❌ No |

| Home loan interest | ₹2,00,000 | ❌ No |

| 80D Health insurance | ₹75,000 | ❌ No |

| 80G Donations | Varies | ❌ No |

| Your own NPS contribution | ₹50,000 | ❌ No |

Key point: Standard deduction of ₹75,000 available for both salaried employees AND pensioners in new regime.

Old Regime — Complete Deductions Guide

Section 123 (Old 80C) — Up to ₹1,50,000

| Investment | Returns | Lock-in | Risk |

|---|---|---|---|

| PPF | 7.1% p.a. | 15 years | Zero |

| ELSS Mutual Funds ✅ | 12-15% (market) | 3 years | Medium |

| EPF | 8.25% p.a. | Till retirement | Zero |

| NSC | 7.7% p.a. | 5 years | Zero |

| Tax Saver FD | 6.5-7.5% | 5 years | Zero |

| Sukanya Samriddhi | 8.2% p.a. | Till daughter age 21 | Zero |

| Life Insurance Premium | Protection tool | Policy term | Zero |

| Home loan principal repayment | NA | Loan tenure | Zero |

ELSS confirmed eligible under Section 123 of ITA 2025. Aggregate limit remains ₹1,50,000.

Home loan bonus: Principal repayment counts within ₹1,50,000 limit AND interest deduction of ₹2,00,000 claimed separately under Section 22. Both simultaneously allowed.

Section 124(3) — NPS Extra Deduction

- Additional ₹50,000 over and above Section 123 limit

- Your own contribution only (not employer’s)

- Old regime only

- Total with Section 123 + NPS = ₹2,00,000

Section 22 — Home Loan Interest

- Up to ₹2,00,000 for self-occupied property

- Includes prior-period interest

- Old regime only

- Claim simultaneously with principal under Section 123

Section 80D — Health Insurance

- Self + family: ₹25,000

- Senior citizen parents: ₹50,000

- Maximum total: ₹75,000

Section 80E — Education Loan Interest

- Full interest deduction — no upper limit

- 8 years from first repayment year

- Old regime only

Section 80G — Donations

- PM Relief Fund: 100% deduction

- Registered charities: 50% deduction

- Old regime only — NOT available in new regime

Big Allowance Increases — FY 2026-27

Income Tax Rules 2026 massively increased allowance limits. These reduce your taxable salary significantly.

| Allowance | Old Limit | New Limit FY 2026-27 | Change |

|---|---|---|---|

| Children Education | ₹100/month per child | ₹3,000/month per child | 30x increase |

| Hostel Allowance | ₹300/month per child | ₹9,000/month per child | 30x increase |

| Free Meals (office) | ₹50 per meal | ₹200 per meal | 4x increase |

| Non-cash Gifts | ₹5,000/year | ₹15,000/year | 3x increase |

| Free Education | ₹1,000/month | ₹3,000/month | 3x increase |

| Medical Loan | ₹20,000 | ₹2,00,000 | 10x increase |

| Overseas Medical | Income < ₹2 lakh | Income < ₹8 lakh | 4x increase |

Ask your employer HR to restructure your salary to include these allowances — immediate tax saving with zero investment.

HRA — Now 8 Cities Get 50%

50% HRA exemption extended from 4 cities to 8 metro cities:

Mumbai · Delhi · Kolkata · Chennai · Bengaluru · Pune · Hyderabad · Ahmedabad

Great news for Hyderabad residents — 50% HRA exemption now available (was 40% earlier).

HRA deduction = lowest of:

- Actual HRA received from employer

- 50% of basic salary (8 metros) / 40% (other cities)

- Actual rent minus 10% of basic salary

Rules:

- Keep monthly rent receipts

- Provide landlord PAN if annual rent exceeds ₹1 lakh

- Cannot claim HRA if living in own house

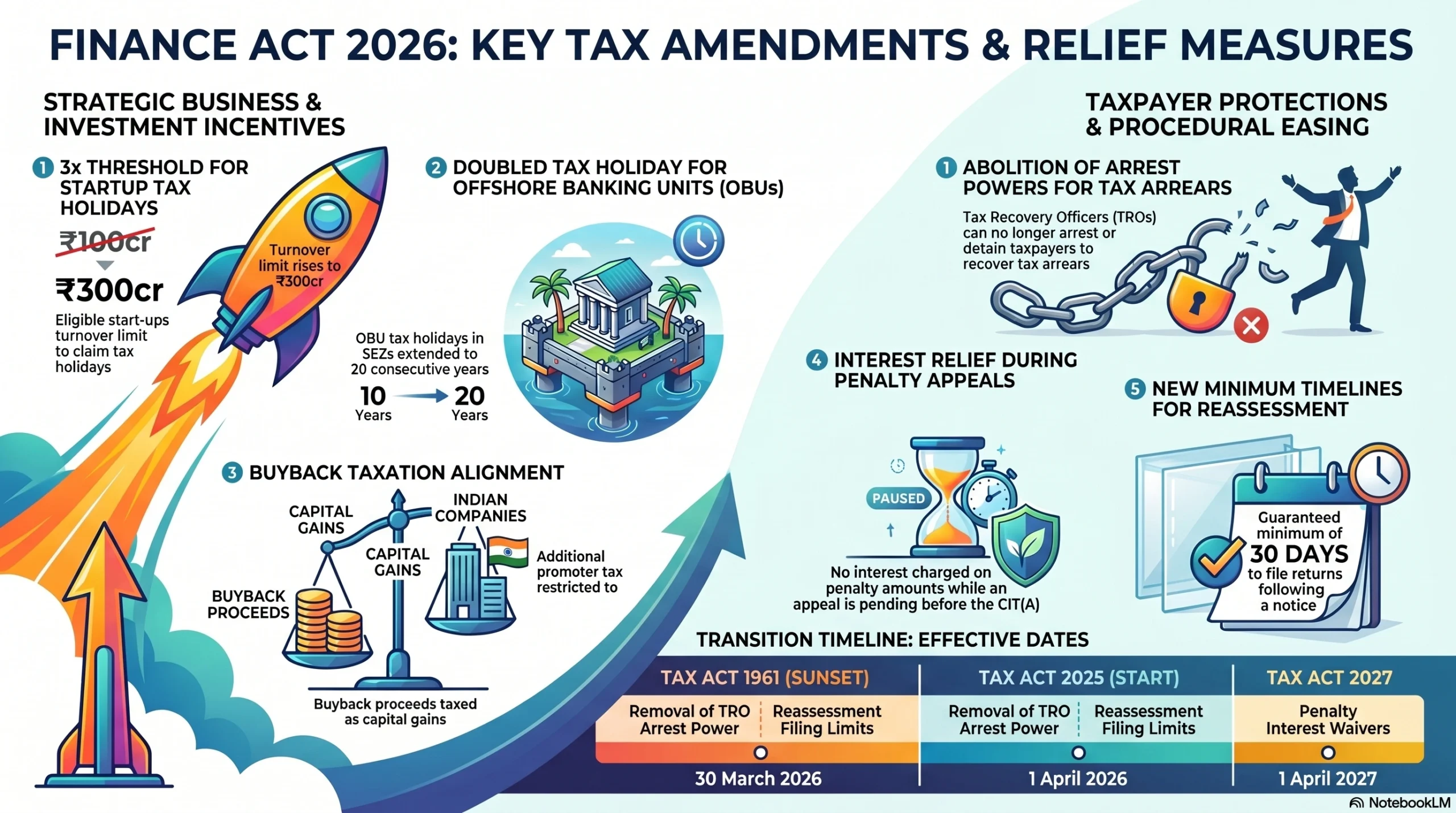

What Got Removed FY 2026-27

| Deduction | Status |

|---|---|

| Dividend interest expense (20%) | ❌ Completely removed for all |

| SGB capital gains exemption — secondary buyers | ❌ Removed |

| SGB exemption — original subscribers held to maturity | ✅ Still available |

| Arrest powers for tax arrears (TROs) | ❌ Abolished from March 30, 2026 |

Crypto Tax FY 2026-27

No change. Still harsh:

- 30% flat tax on all crypto/digital asset gains

- No deduction allowed except cost of acquisition

- Section 87A rebate NOT available on crypto gains

- Even if total income below ₹12 lakh — crypto tax must be paid

- TDS at 1% on crypto transactions above ₹10,000

Late Filing Penalty — Don’t Miss July 31

ITR deadline: July 31, 2026 for salaried individuals.

Miss it? Pay penalty under Section 428:

| Your Income | Late Filing Fee |

|---|---|

| Up to ₹5,00,000 | ₹1,000 |

| Above ₹5,00,000 | ₹5,000 |

Also: Interest under Section 234A at 1% per month on unpaid tax.

New vs Old Regime — Which Saves More?

Choose New Regime if:

- Gross salary up to ₹12,75,000 — zero tax

- No home loan EMI

- Renting but minimal HRA benefit

- Don’t want investment lock-ins

- Want simple filing in minutes

- Business income taxpayer wanting lower rates

Choose Old Regime if:

- Paying home loan interest ₹2 lakh+

- Paying rent in 8 metros — claiming full HRA

- Maxing Section 123 + NPS = ₹2 lakh deduction

- Health insurance for senior citizen parents

- Making large donations under 80G

- Total deductions exceed ₹3,75,000

Quick Calculator:

Add your deductions:

Section 123 (80C) = max ₹1,50,000

NPS Section 124(3) = max ₹50,000

Home loan interest = max ₹2,00,000

80D health insurance = max ₹75,000

HRA = depends on salary/rent

Standard deduction = ₹50,000

If TOTAL > ₹3,75,000 → Old regime wins

If TOTAL < ₹3,75,000 → New regime winsCan you switch every year? Yes — salaried individuals can switch between regimes every year at ITR filing time. Business income taxpayers face restrictions.

Maximum Tax Saving — Old Regime

| Section | Deduction | Notes |

|---|---|---|

| Section 123 (80C) | ₹1,50,000 | ELSS, PPF, EPF etc. |

| Section 124(3) NPS | ₹50,000 | Your own contribution |

| Section 22 (Home loan) | ₹2,00,000 | Self-occupied property |

| Section 80D | ₹75,000 | Self + senior parents |

| Standard deduction | ₹50,000 | Auto-applied |

| HRA | Varies | Metro = 50% of basic |

| Section 80E | No limit | Education loan interest |

| Section 80G | Varies | Donations |

| Total possible | ₹5,25,000+ | Excluding HRA and 80E |

Tax saved on ₹5,25,000 deduction at 30% slab = ₹1,57,500 saved per year.

How to File ITR FY 2026-27

- Visit incometax.gov.in

- Login with PAN

- Select Tax Year 2026-27

- Choose ITR-1 (salaried, income under ₹50 lakh)

- Verify pre-filled data — salary, TDS, Form 26AS

- Add deductions if choosing old regime

- Portal automatically shows tax under both regimes — compare

- Pay remaining tax via challan if any

- E-verify using Aadhaar OTP within 30 days

- Save ITR-V acknowledgement

Deadline: July 31, 2026

Tax Saving Checklist FY 2026-27

- Calculate tax under both regimes — use IT portal’s comparison tool

- Declare regime choice to employer by April 2026

- Invest ₹1,50,000 in ELSS/PPF before March 31, 2027

- Open NPS Tier 1 — extra ₹50,000 deduction

- Buy health insurance for parents — claim 80D

- Submit rent receipts to employer — claim HRA

- Ask HR about children education allowance — now ₹3,000/month

- Ask HR about meal allowance — now ₹200/meal

- Keep donation receipts for 80G

- Submit all investment proofs to employer by February 2027

- File ITR before July 31, 2026

Frequently Asked Questions

Q: Is zero tax really possible on ₹12.75 lakh salary? A: Yes. Under new regime, standard deduction of ₹75,000 reduces taxable income to ₹12,00,000. Section 87A rebate of ₹60,000 equals the tax liability on ₹12 lakh. Result = zero tax payable.

Q: Can I claim 80C investments if I’m in new regime? A: No. Switching to new regime means existing PPF, ELSS, LIC investments remain valid assets — but you cannot claim them as tax deductions. Your money stays safe, just no tax benefit.

Q: I’m a pensioner. Do I get ₹75,000 standard deduction? A: Yes. Standard deduction of ₹75,000 is available to both salaried employees and pensioners under new regime.

Q: What if I miss ITR deadline of July 31? A: You can file belated return until December 31, 2026 with penalty of ₹1,000 (income ≤ ₹5L) or ₹5,000 (income > ₹5L). Plus 1% monthly interest on unpaid tax.

Q: Is crypto taxed even if my income is below ₹12 lakh? A: Yes. Crypto gains are taxed at flat 30% regardless of total income. Section 87A rebate does not apply to crypto gains. No exemption available.

Q: I invested in Sovereign Gold Bonds — is maturity still tax free? A: Only if you are the original subscriber and hold until maturity. Secondary market buyers of SGBs no longer get capital gains exemption from FY 2026-27.

Q: Can I switch from new to old regime next year? A: Yes — if you are salaried or have no business income. You can switch every year at ITR filing. Business income taxpayers need Form 10 IEA and face restrictions on switching back.

Q: I live in Hyderabad and pay rent. What HRA benefit do I get? A: Hyderabad is now in the 8-metro list under ITA 2025. You get 50% HRA exemption (up from 40% earlier). Big benefit for Hyderabad residents.

References

All information in this article sourced from official government documents:

- Income-tax Act, 2025 — incometax.gov.in

- Finance Bill 2026 — indiabudget.gov.in

- Key Features of Budget 2026-27 — finmin.nic.in

- Income Tax Rules 2026 — incometax.gov.in

- PIB Press Release — Budget 2026-27 highlights

- ClearTax — Income Tax Changes from April 2026

- KPMG — Finance Act 2026 Key Amendments

- Grant Thornton — Union Budget 2026 Tax Announcements

Data verified as of April 2026. Tax laws may be updated. Always verify from incometax.gov.in or consult a certified Chartered Accountant before filing.

Disclaimer: This article is for educational purposes only. Kapizo.in is not a tax advisor or CA firm. We are not liable for any financial decisions made based on this content. Always consult a certified CA for personal tax advice.