SIP, or Systematic Investment Plan, is one of the best ways Indians can build long-term wealth. You invest a fixed amount every month, starting from just ₹100, and let compounding grow your money. This guide covers everything you need to know about SIP investing in India for 2026.

This guide uses verified data from SEBI, AMFI and official sources as of April 2026.

Data sources: SEBI Regulations 2026, AMFI data, Perplexity verified April 2026, Economic Times, Groww, Upstox, Bajaj Finserv

What is SIP?

A Systematic Investment Plan (SIP) lets you invest a fixed amount in a mutual fund scheme at regular intervals, weekly, monthly, or quarterly. Instead of timing the market, SIP lets you invest through market cycles automatically.

Example:

- Invest ₹10,000/month in a diversified equity fund

- Over 20 years → grows to approximately ₹1.22 crore

- Based on historical Sensex SIP data

Why SIP works:

- Rupee cost averaging, buy more units when markets fall

- Eliminates need to time the market

- Works on autopilot, deducted from bank automatically

- Start with as little as ₹100/month

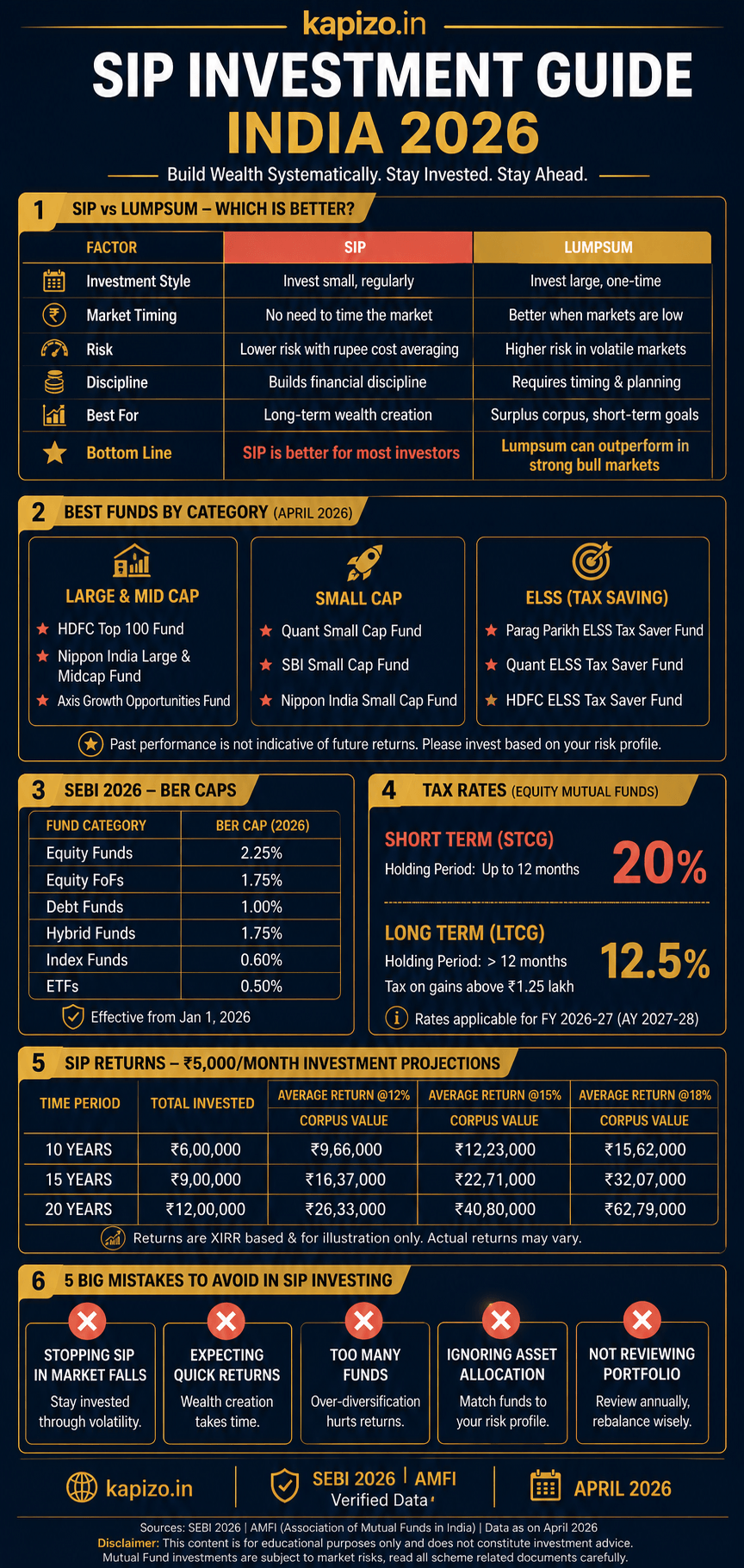

SIP vs Lumpsum, Which is Better?

| Factor | SIP | Lumpsum |

|---|---|---|

| Market timing risk | Low | High |

| Best for volatile markets | ✅ Yes | ❌ Risky |

| Best for rising markets | Moderate | ✅ Better |

| Psychological stress | Low | High |

| Minimum amount | ₹100/month | ₹1,000+ |

| Recommended for beginners | ✅ Yes | ❌ No |

Historical data, Motilal Oswal Midcap Fund:

| Horizon | SIP Returns | Lumpsum Returns | Winner |

|---|---|---|---|

| 5 years | 24.73% CAGR | 29.45% CAGR | Lumpsum |

| 10 years | 22.20% CAGR | 18.77% CAGR | SIP |

Verdict for 2026: Market experts advise against fresh lumpsum investments in mid and small cap funds due to high valuations in early 2026. SIP with 7-10 year horizon = recommended approach.

India Mutual Fund Industry, April 2026

| Metric | Number |

|---|---|

| Total AUM | ₹53+ lakh crore |

| Monthly SIP inflows | ₹26,400+ crore |

| Active SIP accounts | ~10 crore |

India’s mutual fund industry has grown massively. Monthly SIP inflows crossing ₹26,400 crore shows how mainstream SIP investing has become.

Best SIP Funds India, April 2026

Important: Past returns are not guaranteed. Choose based on risk profile and goals. Verify latest NAV and returns from AMFI (amfiindia.com) before investing.

For Beginners, Large & Mid Cap Funds (Balanced Risk)

| Fund | Category | Why Choose |

|---|---|---|

| Mirae Asset Large & Midcap | Large & Mid Cap | Consistent performer, well managed |

| Canara Robeco Large & Mid Cap | Large & Mid Cap | Lower volatility, good track record |

| Axis Large & Mid Cap | Large & Mid Cap | Stable returns, reputed AMC |

| Kotak Large & Midcap | Large & Mid Cap | Good risk-adjusted returns |

Minimum SIP: ₹100 – ₹1,000 depending on fund Note: Mirae Asset Large & Midcap caps SIP at ₹25,000/month

For Aggressive Investors, Small Cap (High Risk, High Return)

| Fund | 5-Year SIP Returns (approx) | Risk |

|---|---|---|

| Quant Small Cap Fund | ~20-25% CAGR | Very High |

| Nippon India Small Cap | ~20-25% CAGR | Very High |

| Bank of India Small Cap | ~20-25% CAGR | Very High |

Warning: Small cap funds are highly sensitive to economic shocks. SIP only, never lumpsum. Minimum 7-10 year horizon required.

For Tax Saving, ELSS Funds

| Fund | Lock-in | Tax Benefit |

|---|---|---|

| Quant ELSS Tax Saver | 3 years | Section 123 (80C) up to ₹1.5L |

| Mirae Asset ELSS | 3 years | Section 123 (80C) |

| Axis ELSS Tax Saver | 3 years | Section 123 (80C) |

ELSS = shortest lock-in (3 years) + tax saving + equity returns

Beginner SIP Strategy, Start Here

Step 1, First SIP portfolio (₹5,000/month):

₹2,500 → Large & Mid Cap fund (stability)

₹1,500 → ELSS fund (tax saving + growth)

₹1,000 → Large Cap index fund (low cost)Step 2, After 1 year (₹10,000/month):

₹3,000 → Large & Mid Cap

₹2,000 → ELSS

₹2,000 → Index fund

₹3,000 → Mid Cap fundStep 3, After 3 years (advanced):

Add small cap exposure (max 20% of portfolio)

Never more than 20% in any single fund

Review portfolio once a year, not monthlySEBI New Regulations 2026, What Changed

SEBI notified new Mutual Fund Regulations in January 2026, effective April 1, 2026. Key changes:

1. New Base Expense Ratio (BER) Framework

Old system: Single TER (Total Expense Ratio) bundled everything. New system: BER covers only core fund costs. Taxes shown separately.

| Fund Type | New BER Cap |

|---|---|

| Equity funds (AUM < ₹500 crore) | 2.10% |

| Equity funds (AUM > ₹50,000 crore) | 0.95% |

| Index funds | 0.90% flat |

| Active equity funds (estimated) | ~1.8% |

| Index funds/ETFs (estimated) | ~0.3-0.5% |

2. What This Means for SIP Investors

- Lower recurring costs = more money stays invested

- Even 0.1% lower annual cost compounds significantly over 10 years

- Direct plans (no distributor) = always cheaper than regular plans

- Compare direct plan BER before investing

3. Mandatory Stress Testing (Small & Mid Cap)

All AMCs must now publish monthly:

- How many days to liquidate 25% of portfolio

- How many days to liquidate 50% of portfolio

- Impact cost for top 20 holdings

Result: Many AMCs have capped fresh lumpsum in small cap funds at ₹2 lakh/day to protect existing investors.

4. Performance-Linked Fees

Fund houses can now link BER to scheme performance, incentivizing fund managers to perform rather than just collect fees.

Mutual Fund Tax, FY 2026-27

Equity Mutual Funds

| Holding Period | Tax Rate | Threshold |

|---|---|---|

| Less than 12 months | 20% (STCG) | No exemption |

| More than 12 months | 12.5% (LTCG) | ₹1.25 lakh exempt |

Example:

- Equity fund gain: ₹2,00,000

- Minus exemption: ₹1,25,000

- Taxable gain: ₹75,000

- Tax at 12.5%: ₹9,375

Debt Mutual Funds

| Purchase Date | Tax Treatment |

|---|---|

| Before 1 April 2023 | LTCG/STCG rules apply |

| After 1 April 2023 | Taxed at income slab rate (no LTCG benefit) |

Practical rule: For tax efficiency, use equity funds for long term. Debt funds taxed like FD for new investments.

ELSS Tax Benefit

- Investment up to ₹1.5 lakh → Section 123 deduction (old regime)

- Gains after 3 year lock-in → taxed as LTCG at 12.5%

- Above ₹1.25 lakh gain threshold

How to Start SIP, Step by Step

- Complete KYC (one-time), Aadhaar + PAN on KRA website

- Choose fund house, SBI, HDFC, Nippon, Mirae, Axis

- Select fund based on risk profile

- Start SIP via:

- Fund house website directly (cheapest)

- Groww / Zerodha Coin / Paytm Money apps

- MF Utility (mfuonline.com), all funds one place

- Set up auto-debit from bank account

- Invest and ignore market noise for 7-10 years

Common SIP Mistakes to Avoid

- Stopping SIP when market falls (worst mistake, this is when you should continue)

- Chasing last year’s top performer (returns rotate between categories)

- Too many funds (5-6 funds = enough for any portfolio)

- Investing in regular plan instead of direct plan (costs 0.5-1% more per year)

- Redeeming before 3+ years (defeats compounding)

- Investing in small cap without 7+ year horizon

SIP Calculator, Quick Reference

Monthly SIP of ₹5,000:

| Rate | 5 years | 10 years | 20 years |

|---|---|---|---|

| 10% p.a. | ₹3.87L | ₹10.33L | ₹38.28L |

| 12% p.a. | ₹4.08L | ₹11.62L | ₹49.96L |

| 15% p.a. | ₹4.45L | ₹13.94L | ₹75.83L |

Use our free SIP calculator → kapizo.in/tools/sip-calculator/

Frequently Asked Questions

Q: What is the minimum SIP amount in India? A: As low as ₹100/month in some funds. Most funds start at ₹500-₹1,000/month. No upper limit for most schemes except some small cap funds which cap at ₹2 lakh/day lumpsum.

Q: Is SIP safe? A: SIP invests in market-linked mutual funds, returns are not guaranteed. However SIP reduces timing risk through rupee cost averaging. Equity SIPs held for 7+ years have historically delivered positive returns in India.

Q: Can I stop SIP anytime? A: Yes. No penalty for stopping SIP anytime (except ELSS which has 3-year lock-in per instalment). Units already purchased remain invested.

Q: SIP vs FD, which is better? A: FD = relatively stable returns (6.5-7.5% now), low-risk. SIP = market linked, higher potential (10-15% historical), but not guaranteed. For goals beyond 5 years, equity SIP historically beats FD significantly.

Q: How many SIPs should I have? A: 3-5 funds is ideal. More than 6-7 funds = over-diversification with no benefit. Each fund should serve a clear purpose (stability, growth, tax saving).

Q: What happens to my SIP if fund house shuts down? A: Your money is safe. Mutual fund assets are held separately by custodians, not by the AMC. SEBI regulations ensure investor assets are protected even if AMC closes.

Disclaimer: Mutual fund investments are subject to market risks. Past returns are not indicative of future performance. Data sourced from SEBI Regulations 2026, AMFI, Economic Times, Groww, Upstox, Bajaj Finserv, verified April 2026. Always read scheme documents carefully and consult a SEBI-registered investment advisor before investing. Kapizo.in may earn affiliate commission from links on this page.