Medical inflation in India is running at 14% per year — double the general inflation rate. A single hospitalisation today can cost ₹2–5 lakh. Without health insurance, one medical emergency can wipe out years of savings.

The good news: India’s health insurance market crossed ₹1,17,505 crore in premiums in FY 2024-25, growing 9.12% year-on-year (IRDAI Annual Report 2024-25). More competition means better plans, lower premiums, and stronger consumer protections than ever before.

This guide gives you everything you need to pick the right health insurance plan in India in 2026 — with verified data from IRDAI, not insurance company marketing.

Why Health Insurance Is Non-Negotiable in 2026

Three numbers tell the story:

- 58 crore Indians are now covered under health insurance (IRDAI 2024-25)

- 264.90 lakh policies issued in FY 2024-25

- Yet large gaps remain — most people are underinsured with covers too small for today’s hospital costs

A ₹2 lakh policy that was “enough” in 2018 does not cover a basic cardiac procedure today. Minimum recommended cover in 2026: ₹5 lakh individual, ₹10 lakh family floater.

Types of Health Insurance in India

1. Individual Health Insurance

Covers one person. Sum insured applies entirely to that individual. Best for: young singles, self-employed professionals.

2026 premium range: ₹6,000–₹12,000/year for a healthy 30-year-old with ₹5 lakh cover.

2. Family Floater

One policy, one sum insured, shared by all family members. Cheaper than buying separate policies. Key risk: one large claim can exhaust the full cover for the year.

2026 premium range: ₹12,000–₹28,000/year for a family of 4 with ₹10 lakh cover.

3. Senior Citizen Health Insurance

Designed for people 60+. Higher premiums but essential. From January 2026, IRDAI rules cap premium hikes for senior citizens at 10% per year — a major consumer protection win.

4. Critical Illness Insurance

Pays a lump sum on diagnosis of specified serious illnesses (cancer, heart attack, stroke, kidney failure). Complements regular health insurance — hospitalisation costs are covered by your main policy, lump sum helps with lost income and recovery costs.

5. Super Top-Up Insurance

Activates after your base policy is exhausted. The deductible applies once per year (not per claim) — making it far better value than a regular top-up. Ideal for people with a ₹5 lakh base policy who want to extend cover to ₹25–50 lakh at low cost.

Best super top-up plans 2026: HDFC ERGO Super Top-up, ICICI Lombard Activate Booster, Niva Bupa Health Recharge, Care Supreme Enhance.

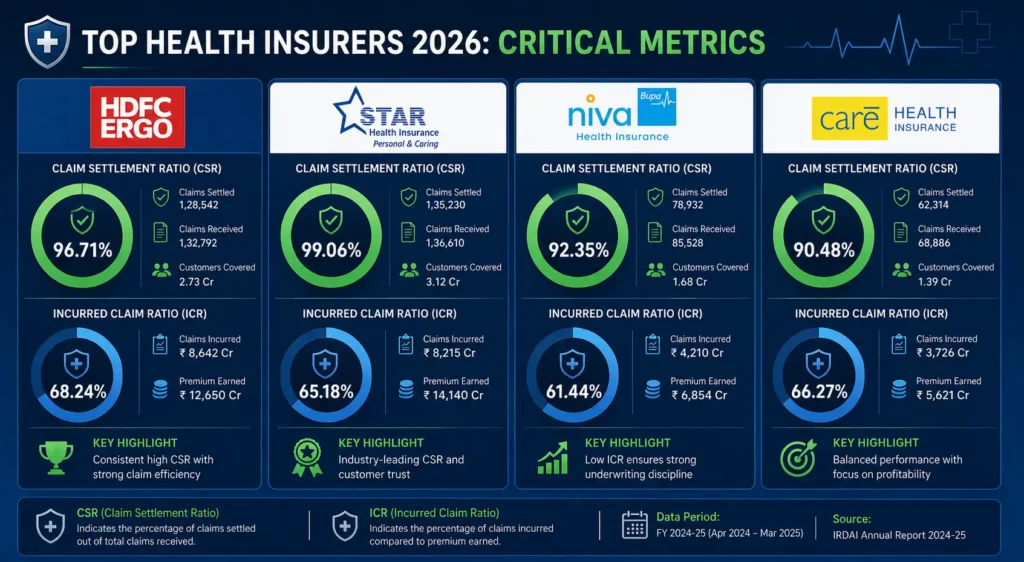

Top Health Insurance Companies in India 2026

Two metrics matter most when comparing insurers:

- Claim Settlement Ratio (CSR) — % of claims settled vs filed (higher = better)

- Incurred Claim Ratio (ICR) — claims paid as % of premiums collected. Between 60–90% is healthy. Too low = insurer keeps too much. Too high = insurer may struggle to pay claims.

Data below: IRDAI Annual Report 2024-25 (ICR) + Perplexity verified sources April 2026 (CSR).

| Company | Type | ICR (FY24-25) | CSR (FY24-25) | Best For |

|---|---|---|---|---|

| Star Health | SAHI | 70.30% | 99.06% | Large hospital network, brand trust |

| HDFC ERGO | Private General | 84.85% | 96.71% | Best overall balance, top-rated plans |

| Niva Bupa | SAHI | 61.22% | Data limited | High sum insured, feature-rich plans |

| Care Health | SAHI | 64.53% | Data limited | Affordable premiums, flexible plans |

| Aditya Birla Health | SAHI | 71.50% | Data limited | Wellness rewards, active health programs |

| ICICI Lombard | Private General | 82.24% | Data limited | Comprehensive coverage, strong network |

| Bajaj Allianz | Private General | 87.31% | Data limited | Good for families, wide coverage |

| New India Assurance | Public Sector | 100.98% | 98.38% | Government trust, pensioners, rural areas |

Source: ICR from IRDAI Annual Report 2024-25 (Statement 10, Page 142). CSR from Perplexity April 2026.

Practical verdict:

- Best all-round: HDFC ERGO

- Best CSR: Star Health (99.06%)

- Best for affordability: Care Health

- Best for high cover: Niva Bupa

How Much Cover Do You Actually Need?

| Situation | Recommended Cover | Estimated Premium/Year |

|---|---|---|

| Single, age 25-35, metro city | ₹10 lakh individual | ₹8,000–₹15,000 |

| Family of 3-4, age 30-45 | ₹15–20 lakh floater | ₹18,000–₹32,000 |

| Senior citizens (60+) | ₹10 lakh minimum | ₹30,000–₹60,000+ |

| Any age with existing base policy | ₹25–50 lakh super top-up | ₹5,000–₹12,000 add-on |

Premium estimates: Perplexity April 2026. Actual premiums vary by insurer, city, and health status.

Section 80D Tax Benefit — What You Can Save

Health insurance premiums are tax deductible under Section 80D of the Income Tax Act. This applies only under the Old Tax Regime. No 80D benefit under the New Tax Regime.

Finance Bill 2026 made no changes to 80D limits. Current limits for FY 2026-27:

| Who is Covered | Max Deduction |

|---|---|

| Self + spouse + dependent children (all below 60) | ₹25,000 |

| Self/family includes a senior citizen | ₹50,000 |

| Parents below 60 | ₹25,000 additional |

| Senior citizen parents | ₹50,000 additional |

| Preventive health check-up | Up to ₹5,000 (within overall limit) |

| Maximum possible deduction | ₹1,00,000 (self + senior parents, both 60+) |

Example: You are 35, paying ₹20,000 premium for self + family. Parents are senior citizens, you pay ₹35,000 for them. Total 80D deduction: ₹20,000 + ₹35,000 = ₹55,000. At 30% tax bracket, you save ₹16,500 in tax.

Key IRDAI Rules You Must Know (2025-26)

Major consumer protections now in force:

- Cashless claim pre-authorisation: Insurers must respond within 1 hour

- Discharge approval: Must be given within 3 hours

- 60-month moratorium: After 5 continuous years, your insurer cannot deny a claim due to non-disclosure (unless fraud is proven)

- 30-day free-look period: For annual and longer policies — return if not satisfied

- AYUSH parity: Ayurveda, Yoga, Unani, Siddha, Homeopathy treatments must be covered at par with allopathy

- Senior citizen premium cap: Insurers cannot raise premiums for senior citizens by more than 10% per year (from January 2025)

- Bima-ASBA: New UPI-based premium blocking — funds only debited after policy is issued

- Customer Information Sheet (CIS): Every policy must include a plain-language summary of key terms, exclusions, and portability rights

What to Check Before Buying

Do not buy based on premium alone. Check all of these:

- Room rent limit: Many plans cap room rent at 1-2% of sum insured. A ₹5,000/night cap in a ₹10,000/night hospital means proportional deductions across your entire bill.

- Co-payment clause: Some plans require you to pay 10-30% of every claim. Avoid if possible.

- Waiting period: Pre-existing diseases usually have 2-4 year waiting periods. Check this carefully if you have any existing conditions.

- Sub-limits: Caps on specific treatments (cataract, maternity, etc.) can leave you underinsured.

- Network hospitals: Cashless claims only work at network hospitals. Check your preferred hospital is included.

- No-claim bonus: Good plans increase your sum insured by 10-50% for every claim-free year.

- Restoration benefit: Sum insured gets restored after a claim — critical for family floater policies.

Health Insurance Market — 2024-25 at a Glance

- Total health insurance premium: ₹1,17,505 crore (9.12% growth)

- Standalone Health Insurers (SAHI) fastest growing: 16% growth

- Total policies issued: 264.90 lakh

- Lives covered: 58 crore

- Industry-wide claim settlement rate: ~87.5% (326 lakh claims paid out of 372.58 lakh processed)

Source: IRDAI Annual Report 2024-25.

Our Recommendation by Profile

| Profile | Recommended Plan Type | Suggested Insurer |

|---|---|---|

| Young single, 25-30 | Individual ₹10L + Super Top-up | Care Health / Niva Bupa |

| Young family, 30s | Family Floater ₹15-20L | HDFC ERGO / Star Health |

| Age 45+ with parents | Individual ₹10L + Senior Citizen plan for parents | Star Health / HDFC ERGO |

| Corporate employee | Super Top-up over group cover | HDFC ERGO / ICICI Lombard |

| Budget-conscious | ₹5L base + ₹20L Super Top-up | Care Health / Niva Bupa |

Final Word

Health insurance is not an expense — it is the financial safety net that protects everything else you are building. With IRDAI’s new consumer protections, mandatory cashless processing timelines, and the 60-month moratorium rule, 2026 is one of the best times to buy or upgrade your cover.

Start with the minimum: ₹10 lakh individual or ₹15 lakh family floater. Add a super top-up to extend cover without a large premium jump. And if you are on the old tax regime, claim your full Section 80D deduction every year.

Compare health insurance plans on PolicyBazaar, Ditto, or direct insurer websites. Always check the final quote with your exact age and city — advertised premiums can vary significantly.

Compare health insurance plans: Use PolicyBazaar or Ditto to compare premiums for your age and city. Takes 2 minutes and shows verified quotes from 15+ insurers.

Frequently Asked Questions

Which health insurance company has the highest claim settlement ratio in India in 2025-26?

Based on FY 2024-25 data, Star Health Insurance has the highest CSR at 99.06%, followed by New India Assurance at 98.38% and HDFC ERGO at 96.71%. Note that Standalone Health Insurers (SAHI) like Star Health, Niva Bupa, and Care Health publish company-level CSR, while general insurers report health segment data differently. Always cross-check CSR with the Incurred Claim Ratio (ICR) for a complete picture.

How much does health insurance cost in India in 2026?

For a healthy 30-year-old, a ₹5 lakh individual cover costs roughly ₹6,000–₹12,000 per year. A family floater with ₹10 lakh cover for 4 members costs approximately ₹12,000–₹28,000 per year. Premiums vary based on your age, city of residence, chosen insurer, room rent limits, and add-ons. Use insurer premium calculators for an exact quote.

Is Section 80D still available in 2026-27?

Yes. Section 80D deductions are unchanged for FY 2026-27. The Finance Bill 2026 made no changes to 80D limits. You can claim up to ₹25,000 for self and family (₹50,000 if senior citizen), plus up to ₹50,000 additional for senior citizen parents. Maximum possible deduction is ₹1,00,000. Important: 80D is only available under the Old Tax Regime.

What is the difference between a super top-up and a regular top-up health insurance plan?

A regular top-up applies the deductible per claim — you must exceed the threshold on every single hospitalisation for the top-up to activate. A super top-up applies the deductible once per policy year — after your cumulative claims for the year exceed the deductible, the plan covers everything above that. For families with multiple smaller claims in a year, super top-up is almost always better value.

What are the new IRDAI health insurance rules in 2025-26?

Key new rules: Cashless pre-authorisation must be given within 1 hour, and discharge approval within 3 hours. Senior citizen premium hikes are capped at 10% per year. After a 60-month moratorium, claims cannot be denied for non-disclosure. AYUSH treatments (Ayurveda, Yoga, etc.) must be covered at par with allopathy. Every policy must now include a Customer Information Sheet (CIS) summarising exclusions in plain language.

Should I buy a family floater or separate individual health policies?

A family floater is cheaper upfront — one policy covers all members at lower combined premium than separate plans. The risk: the entire sum insured is shared, so one large claim leaves less cover for others in that year. If you have senior parents (60+), do not include them in a family floater — buy them a separate senior citizen plan. For young families with no major health history, a floater with a restoration benefit is usually the best value.