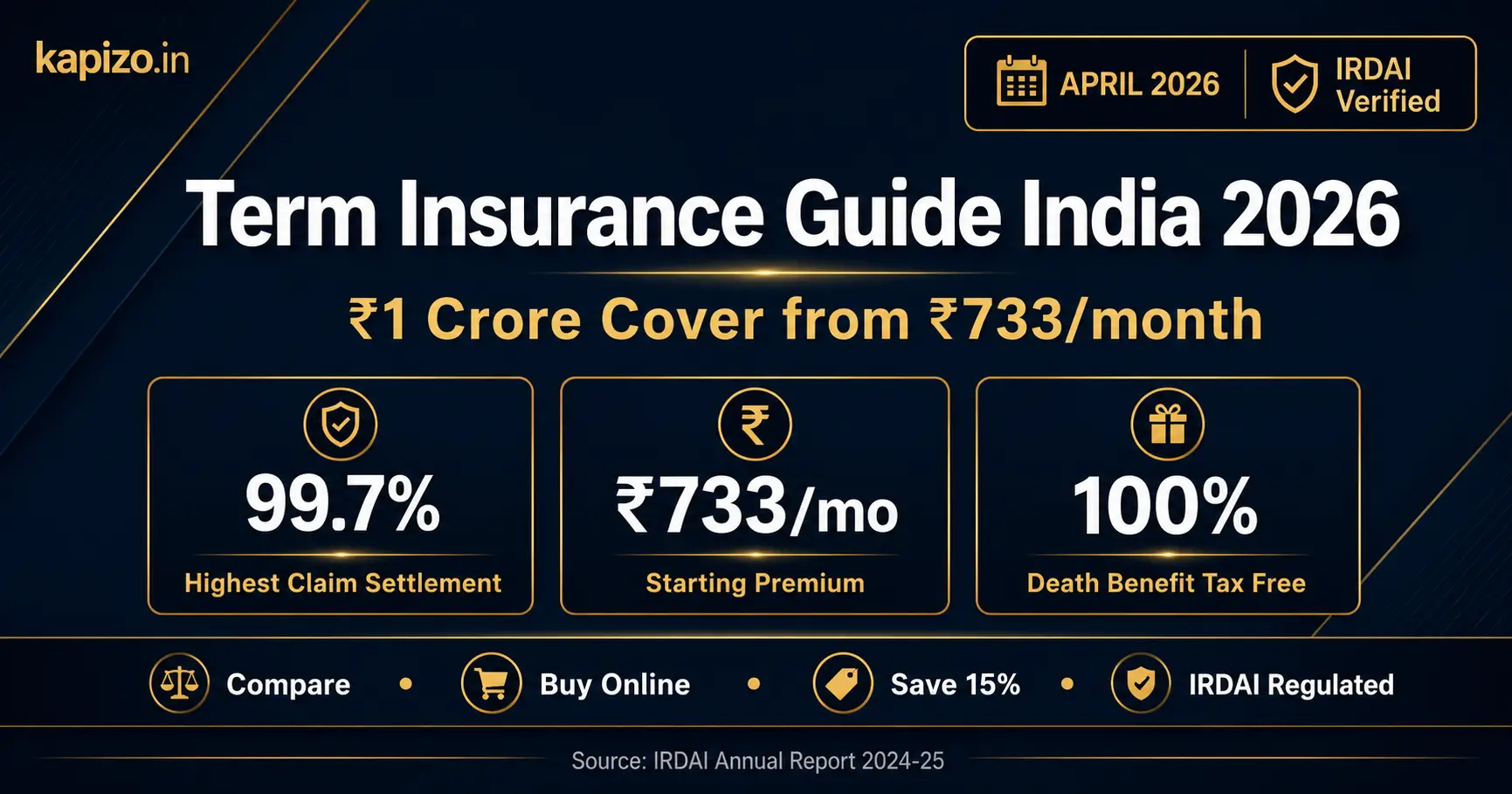

Term insurance is the most important financial product every Indian should buy. Yet most people either don’t have it or are dangerously underinsured. This guide explains everything simply so you can make the right decision for your family.

All claim settlement ratios in this article are from IRDAI Annual Report 2024-25, the latest available as of April 2026.

What is Term Insurance?

Term insurance is pure life insurance. You pay a small premium every year. If you die during the policy term, your family gets the full sum assured (coverage amount). If you survive, nothing is paid, no maturity benefit.

Why this is actually good:

- Premiums are very low (₹700-1,200/month for ₹1 crore cover)

- 100% of premium goes toward protection

- Simple, transparent, no hidden charges

- Family gets full amount tax-free

How Much Coverage Do You Need?

Standard formula: 10-15 times your annual income

| Annual Income | Minimum Coverage |

|---|---|

| ₹3,00,000 | ₹30-45 lakh |

| ₹5,00,000 | ₹50-75 lakh |

| ₹8,00,000 | ₹80 lakh – 1.2 crore |

| ₹12,00,000 | ₹1.2 – 1.8 crore |

| ₹20,00,000 | ₹2 – 3 crore |

Also consider:

- Outstanding loans (home loan, car loan)

- Children’s education costs

- Parents’ medical expenses

- Family’s monthly expenses for 15-20 years

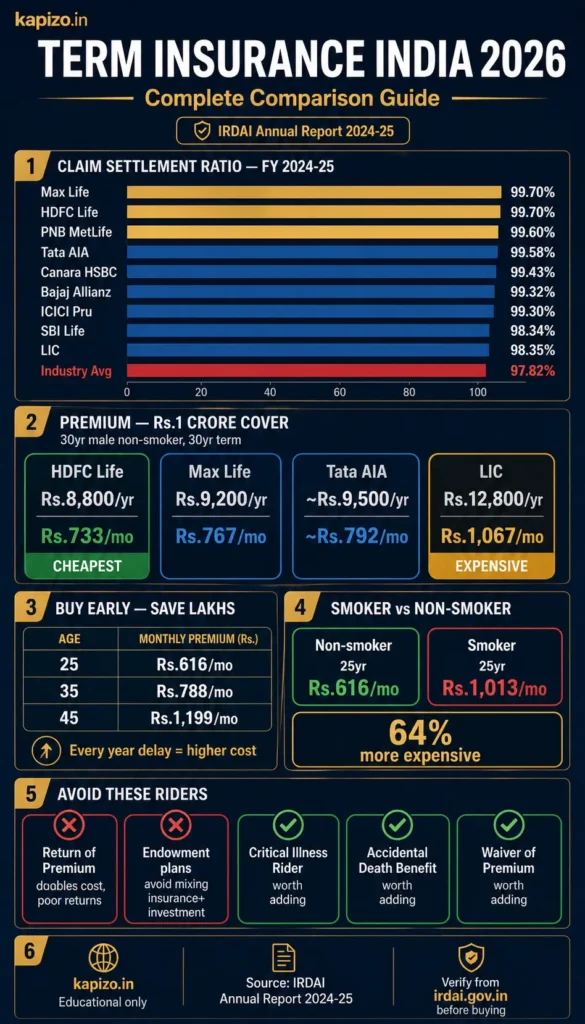

Best Term Insurance Plans India 2026

| Insurer | Claim Settlement Ratio | Verdict |

|---|---|---|

| Axis Max Life | 99.70% | Best |

| HDFC Life | 99.70% – 99.80% | Best |

| PNB MetLife | 99.60% | Excellent |

| Tata AIA | 99.41% – 99.58% | Excellent |

| Canara HSBC | 99.43% | Excellent |

| Bajaj Allianz | 99.32% | Very Good |

| ICICI Prudential | 99.30% | Very Good |

| SBI Life | 98.34% – 99.40% | Good |

| LIC | 98.35% | Good |

Source: IRDAI Annual Report 2024-25

Industry average: 97.82%

Choose insurer with CSR above 97%

Top private insurers now settle 99%+ claims, significantly better than industry average. HDFC Life achieved its highest-ever ratio in FY25. Always verify latest CSR from irdai.gov.in before buying any plan.

Sample Premium – Rs.1 Crore Cover

30-year-old male non-smoker, 30-year term

| Insurer | Annual Premium | Monthly |

|---|---|---|

| HDFC Life | Rs.8,800 – Rs.13,500 | Rs.733 – Rs.1,125 |

| Max Life | Rs.9,200 – Rs.15,200 | Rs.767 – Rs.1,267 |

| Tata AIA | Competitive | Around Rs.800-900 |

| LIC Tech Term | Rs.12,800 – Rs.18,200 | Rs.1,067 – Rs.1,517 |

HDFC Life and Max Life give best value. LIC is most expensive but government backed.

Term Insurance vs Other Life Insurance

| Type | Premium | Coverage | Returns | Recommended? |

|---|---|---|---|---|

| Term Insurance | Very Low | Very High | Zero (pure protection) | ✅ YES |

| Endowment/Money Back | Very High | Low | 4-6% (poor) | ❌ NO |

| ULIP | High | Medium | Market-linked | ❌ Mostly NO |

| Whole Life | High | Medium | Some | ❌ NO |

Golden rule: Buy term insurance for protection. Invest separately in mutual funds for wealth creation. Never mix insurance and investment.

Riders: Should You Add Them?

Riders are optional add-ons to your term plan:

| Rider | What it does | Worth it? |

|---|---|---|

| Critical Illness Rider | Lump sum on 36+ critical illnesses | ✅ YES |

| Accidental Death Benefit | Extra payout on accidental death | ✅ YES |

| Waiver of Premium | Future premiums waived on disability | ✅ YES |

| Return of Premium | Get all premiums back if you survive | ❌ NO (doubles cost) |

Avoid Return of Premium rider. It doubles your premium but effective return is only 5-6% which is worse than FD or mutual funds.

How to Buy Term Insurance: Step by Step

Option 1: Direct from Insurer (Cheapest)

- Visit insurer website directly

- Use online premium calculator

- Fill health declaration honestly

- Pay premium online

- Policy issued within 24-48 hours

Option 2: Via Aggregator

- Visit Policybazaar or Coverfox

- Compare multiple plans simultaneously

- Choose best plan

- Redirected to insurer for purchase

Both options same premium. Aggregator doesn’t cost extra.

Medical Tests: When Required?

| Sum Assured | Medical Test |

|---|---|

| Up to ₹50 lakh | Usually no test (online declaration) |

| ₹50 lakh – ₹1 crore | Basic blood test + BMI |

| Above ₹1 crore | Full medical examination |

| Any amount (age 45+) | Medical test usually required |

Don’t hide health conditions. Non-disclosure = claim rejection = family gets nothing. Always declare pre-existing conditions honestly.

Most Common Reasons Claims Get Rejected

- Non-disclosure: hiding smoking, medical history, occupation

- Policy lapse: missing premium payments

- Wrong nominee details: name mismatch in documents

- Suicide within first year: excluded in most policies

- Fraud: misrepresentation of income or age

To ensure claim never gets rejected:

- Disclose everything honestly at purchase

- Set up auto-debit for premium

- Update nominee details if family changes

- Keep policy documents safely + share location with family

Tax Benefits on Term Insurance

- Section 80C (Old Regime): Premium up to ₹1.5 lakh deductible

- Section 10(10D): Death benefit received by family = 100% tax-free

- New Regime: 80C not available but death benefit still tax-free

When Should You Buy Term Insurance?

The earlier the better.

How Age Affects Premium (Rs.1 Crore, Non-Smoker)

| Age | Monthly Premium | Annual Premium |

|---|---|---|

| 18-24 yrs | Rs.400 – Rs.434 | Around Rs.5,000 |

| 25 yrs | Rs.522 – Rs.616 | Around Rs.7,500 |

| 35 yrs | Around Rs.788 | Around Rs.13,750 |

| 45 yrs | Around Rs.1,199 | Around Rs.33,500 |

Smoker penalty: 25-year-old smoker pays Rs.1,013/month vs Rs.616 non-smoker = 64% more

Source: IRDAI Annual Report 2024-25 and insurer disclosures verified April 2026

Every year you delay = higher premium for same coverage.

Buy term insurance when you have:

- Dependents (spouse, children, parents)

- Outstanding loans

- Started earning

Frequently Asked Questions

Q: Which is the best term insurance plan in India 2026? A: Max Life Smart Secure Plus has highest claim settlement ratio at 99.51%. HDFC Life Click 2 Protect and Tata AIA are also excellent. Best plan depends on your age, health, and coverage needed.

Q: How much term insurance do I need? A: Minimum 10-15 times annual income. Also add outstanding loans and future education costs. For ₹8 lakh annual income. minimum ₹80 lakh to ₹1 crore coverage.

Q: Is LIC better than private insurers for term insurance? A: LIC has 98.62% claim settlement ratio. Comparable to top private insurers. LIC has government backing = zero insolvency risk. But private insurers often cheaper and faster. Both are safe options.

Q: Can I buy term insurance with pre-existing conditions? A: Yes. You must declare all conditions. Insurer may charge higher premium or exclude specific conditions. Never hide health conditions. leads to claim rejection.

Q: What happens if I stop paying premium? A: Policy lapses after grace period (usually 30 days). No coverage during lapse. Can be revived within 2-5 years by paying pending premiums + interest. Set auto-debit to never miss payment.

Q: Is term insurance premium tax deductible? A: Yes under old tax regime. Section 80C up to ₹1.5 lakh. Death benefit always 100% tax-free under Section 10(10D) regardless of regime.

Q: Should I buy term insurance online or offline? A: Online = cheaper (10-15% lower premium) + instant policy. Offline agent = hand-holding during claim. For most people online is better. claim process now fully digital.

Disclaimer: Claim settlement ratios sourced from IRDAI Annual Report 2024-25. Premiums mentioned are indicative only. actual premiums vary by age, health and insurer. Always verify from official insurer websites or irdai.gov.in. Kapizo.in may earn affiliate commission from links. Not financial advice. Consult a certified insurance advisor for personalised guidance.