Your credit score is a 3-digit number that controls your financial life in India. It decides whether you get a loan, what interest rate you pay, and even whether your rental application gets approved. Yet most Indians have never checked their credit score.

This guide explains everything about credit scores in India, how they work, which bureau matters most, and how to improve yours starting today.

What is a Credit Score?

A credit score is a number between 300 and 900 that represents how trustworthy you are as a borrower. Banks and NBFCs check this score before approving any loan or credit card application.

Higher score = lower risk for lender = better loan terms for you.

4 Credit Bureaus in India

India has 4 SEBI-regulated credit bureaus. Each maintains your credit report independently.

| Bureau | Score Name | Range | Most Used By |

|---|---|---|---|

| TransUnion CIBIL | CIBIL Score | 300-900 | Most banks and NBFCs |

| Experian | Experian Score | 300-900 | HDFC Bank, Kotak |

| CRIF High Mark | CRIF Score | 300-900 | Microfinance, rural lenders |

| Equifax | Equifax Score | 300-900 | Some NBFCs and banks |

Which bureau matters most? CIBIL is checked by 90%+ of Indian lenders. Focus on CIBIL first. Other bureau scores usually move in same direction.

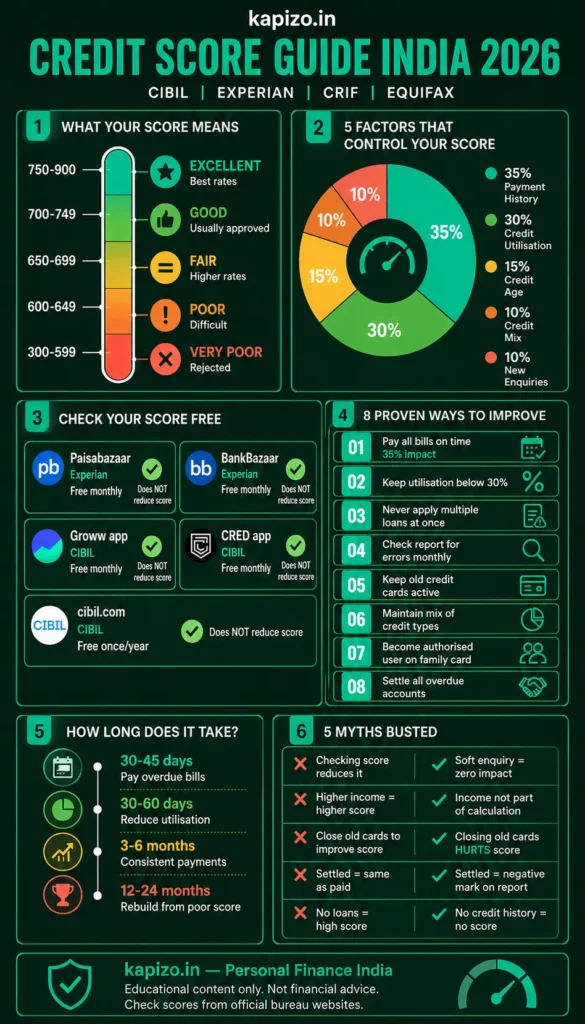

Credit Score Ranges. What They Mean

| Score Range | Rating | What it Means | Loan Approval |

|---|---|---|---|

| 750 – 900 | Excellent | Best rates, easy approval | Almost certain |

| 700 – 749 | Good | Usually approved | Very likely |

| 650 – 699 | Fair | Higher interest rate | Possible with conditions |

| 600 – 649 | Poor | Difficult approval | Unlikely |

| 300 – 599 | Very Poor | Usually rejected | Very unlikely |

Target score: 750 and above for best loan rates and easy approvals.

What Affects Your Credit Score

| Factor | Weightage | What to Do |

|---|---|---|

| Payment history | 35% | Never miss EMI or credit card payment |

| Credit utilisation | 30% | Use less than 30% of credit card limit |

| Credit age | 15% | Keep old credit cards active |

| Credit mix | 10% | Have both secured and unsecured loans |

| New enquiries | 10% | Avoid multiple loan applications |

How to Check Credit Score Free in India

You are legally entitled to one free credit report per year from each bureau. Here are the best free options:

| Platform | Bureau | Cost | Frequency |

|---|---|---|---|

| cibil.com | CIBIL | Free once/year | Annual |

| Paisabazaar | Experian | Free unlimited | Monthly |

| BankBazaar | Experian | Free unlimited | Monthly |

| Groww app | CIBIL | Free | Monthly |

| CRED app | CIBIL | Free | Monthly |

| OneScore app | Experian | Free unlimited | Monthly |

Checking your own score is a soft inquiry and does NOT reduce your score. Check monthly.

8 Proven Ways to Improve Credit Score

1. Pay All Bills on Time. Every Time

Payment history = 35% of your score. One missed payment drops score by 50-100 points immediately. Set up auto-debit for all EMIs and credit card minimum dues. Never rely on memory.

2. Keep Credit Utilisation Below 30%

If your credit card limit is Rs.1,00,000, never spend more than Rs.30,000 in a billing cycle. High utilisation signals financial stress to lenders. Request limit increase from bank if needed.

3. Never Apply for Multiple Loans at Once

Every loan application triggers a hard enquiry on your report. Multiple hard enquiries in a short period can drop your score. It also looks desperate to lenders. Space applications minimum 6 months apart.

4. Check Your Credit Report for Errors

Millions of Indians have errors in their credit report. Closed loans may show as active. Wrong personal details or late payments marked incorrectly are common issues. Check free at Paisabazaar monthly. Raise dispute online at cibil.com if errors found. Correction takes 30-45 days.

5. Keep Old Credit Cards Active

Credit age = 15% of score. Older credit history means a better score. Never close your oldest credit card even if you rarely use it. Make one small purchase every 3 months to keep it active.

6. Maintain a Mix of Credit Types

Having both secured loans (home, car) and unsecured credit (credit cards, personal loan) shows responsible credit behaviour. This helps score improve over time. Do not take loans just for this purpose though.

7. Become an Authorised User

Ask a family member with excellent credit score to add you as authorised user on their credit card. Their good payment history reflects on your report. Score can improve within 1-2 billing cycles.

8. Settle or Close All Overdue Accounts

Overdue accounts damage score more than anything else. Call the bank, negotiate settlement amount, pay it, and get a No Objection Certificate in writing. Score starts recovering within 3-6 months after settlement.

How Long Does It Take to Improve Score?

| Action | Time to See Impact |

|---|---|

| Pay overdue bills immediately | 30-45 days |

| Reduce credit card utilisation | 30-60 days |

| Dispute and fix errors | 30-45 days |

| Consistent on-time payments | 3-6 months |

| Rebuild from very poor score | 12-24 months |

Hard Enquiry vs Soft Enquiry

| Type | What Triggers It | Affects Score? |

|---|---|---|

| Hard enquiry | You apply for loan or credit card | Yes, drops score slightly |

| Soft enquiry | You check your own score | No impact at all |

| Soft enquiry | Bank checks for pre-approved offer | No impact at all |

Hard enquiries stay on report for 2 years but impact reduces after 6 months.

Credit Score Myths. Busted

Myth 1: Checking my score reduces it.

Fact: Checking your own score = soft enquiry = zero impact.

Myth 2: Higher income = higher credit score.

Fact: Income is not part of credit score calculation. Payment behaviour is what matters.

Myth 3: Closing old credit cards improves score.

Fact: Closing old cards reduces credit age and available limit. Score usually drops.

Myth 4: Settling a loan is same as paying it fully.

Fact: Settled status on report = negative mark. Pay in full whenever possible.

Myth 5: I have no loans so my score must be high.

Fact: No credit history = no score or very low score. You need some credit activity to build a score.

How to Build Credit Score from Zero

If you have no credit history:

- Get a secured credit card (backed by FD. Banks give this easily)

- Use it for small purchases monthly

- Pay full bill before due date every month

- After 6-12 months, apply for regular credit card

- Score builds naturally through this process

Best secured credit cards for beginners: SBI Advantage Plus, ICICI Instant Platinum, Axis Insta Easy.

Credit Score for Different Financial Products

| Product | Minimum Score | Best Rate Score |

|---|---|---|

| Home loan | 700+ | 750+ |

| Personal loan | 700+ | 750+ |

| Car loan | 680+ | 740+ |

| Credit card | 680+ | 750+ |

| Business loan | 700+ | 760+ |

| Education loan | 650+ | 720+ |

Frequently Asked Questions

Q: What is a good credit score in India?

750 and above is considered excellent. Most banks approve loans easily and offer best interest rates to people with 750+ score. Anything above 700 is considered good and usually gets approval.

Q: How often is credit score updated?

Credit bureaus update scores every 30-45 days based on information submitted by lenders. When you pay EMI or credit card bill, lender reports to bureau within 30-45 days.

Q: Does credit score affect job applications?

Some employers, especially in banking and finance sector, check credit history as part of background verification. Poor credit score can affect job prospects in financial services.

Q: Can I have different scores from different bureaus?

Yes. Each bureau calculates score independently using slightly different algorithms. Scores can vary by 20-50 points between bureaus. CIBIL score is most widely used by Indian lenders.

Q: What happens to credit score after bankruptcy or loan settlement?

Both significantly damage credit score for 7-10 years on record. Settlement shows as negative mark. Recovery is possible but takes 2-3 years of consistent good behaviour minimum.

Q: Is 650 credit score enough for home loan?

Some lenders approve at 650 but with higher interest rate and stricter conditions. Most prefer 700+. Best rates need 750+. Focus on improving score to 750 before applying for large loans.

Disclaimer: Credit score information is for educational purposes only. Scores vary by bureau and individual credit history. Always check your score from official bureau websites. Kapizo.in may earn affiliate commission from links on this page. Not financial advice.