Last Updated: May 2026

– CIBIL score below 700 = loan rejections, higher interest rates

– Payment history alone controls 35% of your score

– Most Indians can reach 750+ within 6–12 months with consistent action

– You are legally entitled to 1 free CIBIL report per year

– No company can “fix” your score for money — those are scams

– Four bureaus in India: CIBIL (TransUnion), Experian, CRIF, Equifax — all matter

If your loan application was rejected last week or your credit card limit is stuck at ₹50,000 while your colleague got ₹3 lakh — your credit score is the reason. In India, a score below 700 closes doors to good interest rates, higher limits, and fast approvals.

The frustrating part is that most people do not know exactly which actions hurt their score, which help it, and how long real recovery takes. This guide covers all of it — with specific numbers, timelines, and scenarios based on how Indian credit bureaus actually calculate scores.

What is a CIBIL Score and Why Do Banks Care So Much?

A CIBIL score is a 3-digit number between 300 and 900 generated by TransUnion CIBIL — India’s oldest and most widely used credit bureau. It summarises your entire credit history into a single number that tells lenders how likely you are to repay a loan on time.

When you apply for a home loan, personal loan, car loan, or credit card, the lender pulls your CIBIL report within seconds. If your score is below their threshold — usually 700 for most banks, 750 for best rates — the system flags your application before a human even looks at it.

India has four licensed credit bureaus: TransUnion CIBIL, Experian, CRIF High Mark, and Equifax. All four collect data from banks and NBFCs and generate separate scores. HDFC Bank might use CIBIL. Bajaj Finance uses CRIF. Your score may differ slightly between bureaus — but the underlying data is largely the same.

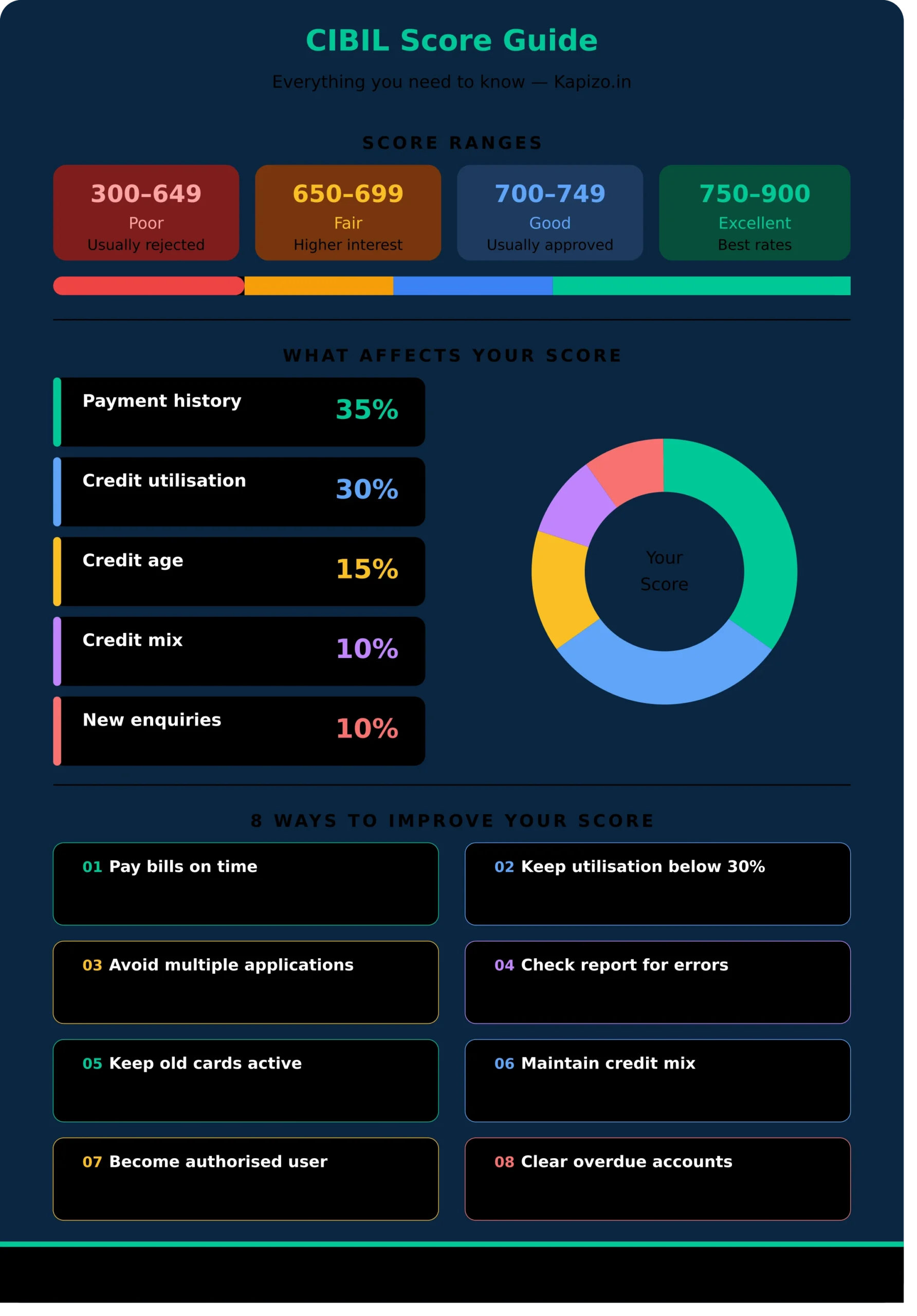

CIBIL Score Range — What Your Number Actually Means

| Score Range | Rating | Real-World Impact |

|---|---|---|

| 800 – 900 | Exceptional | Pre-approved offers, lowest interest rates, instant approvals |

| 750 – 799 | Excellent | Easy approval at most banks, competitive rates |

| 700 – 749 | Good | Usually approved, may get slightly higher rates |

| 650 – 699 | Fair | Selective approvals, significantly higher interest |

| 600 – 649 | Poor | Mostly rejected by banks, only NBFCs may approve |

| 300 – 599 | Very Poor | Almost always rejected, rebuilding required |

| -1 or NH | No History | No credit taken yet — treated with caution by lenders |

What NH means: If you have never taken a loan or credit card, your score shows as -1 or NH (No History). This is not the same as a bad score — but banks are cautious about lending to someone with no track record. Building credit from zero requires a different strategy than rebuilding from a poor score.

What Factors Affect Your CIBIL Score — With Real Weightage

| Factor | Weightage | What Hurts | What Helps |

|---|---|---|---|

| Payment History | 35% | Late payments, defaults, settlements | Every EMI and bill paid on time |

| Credit Utilisation | 30% | Using more than 30% of credit limit | Keeping usage below 30% consistently |

| Credit Age | 15% | Closing old accounts, short history | Keeping oldest accounts open |

| Credit Mix | 10% | Only one type of credit | Mix of secured + unsecured loans |

| New Enquiries | 10% | Multiple loan applications at once | Applying only when necessary |

Payment history and credit utilisation together control 65% of your score. If you fix only these two things, your score will improve. Everything else is fine-tuning.

10 Proven Steps to Improve Your CIBIL Score

Step 1 — Pay Every EMI and Credit Card Bill on Time, Always

This is not optional. Payment history is 35% of your score. A single missed EMI can drop your score by 50–100 points overnight. Two missed payments can push you from 750 to below 650.

Action: Set up auto-pay for at least the minimum amount due on all credit cards. Set up standing instructions for all EMIs. Check bank account balance 3 days before every due date. One bounced auto-pay is as damaging as a manual miss.

Real impact: If you have been missing payments and start paying on time consistently, you can see 40–80 point improvement within 3–6 months as the positive payment data accumulates.

Step 2 — Reduce Credit Utilisation Below 30%

Credit utilisation is the percentage of your total credit card limit you are using. If your total limit across all cards is ₹2,00,000 and your total outstanding is ₹80,000 — your utilisation is 40%. That is hurting your score.

The target is below 30% overall. Below 10% is ideal if you want a score above 800.

Three ways to reduce utilisation fast:

- Pay down existing balances — most effective

- Request a credit limit increase from your bank without increasing spending

- Spread spending across multiple cards instead of concentrating on one

Real impact: Reducing utilisation from 60% to 25% can improve your score by 40–70 points within one billing cycle — typically 30–45 days.

Step 3 — Get Your Free CIBIL Report and Check for Errors

This step is underused and extremely important. According to consumer complaints data, a significant number of Indian credit reports contain errors — closed loans still showing as active, wrong personal details, accounts that do not belong to you.

You are legally entitled to one free credit report per year from each bureau under RBI guidelines.

How to get your free CIBIL report:

- Go to cibil.com

- Click “Get Free Credit Score”

- Enter PAN, date of birth, mobile number

- Verify OTP

- Download full report — free once per year

Common errors to look for:

- Loan accounts marked as “Written Off” that you actually paid

- Settled accounts still showing outstanding balance

- Hard enquiries you did not authorise

- Wrong name, address, or PAN linked to your profile

- Duplicate accounts listed twice

How to raise a CIBIL dispute: Log in to cibil.com → Dispute Centre → Select the incorrect item → Submit with supporting documents (bank NOC, payment receipts). CIBIL must resolve the dispute within 30 days under RBI guidelines. If resolved in your favour, the error is removed and your score updates within 45 days.

Step 4 — Never Apply for Multiple Loans at the Same Time

Every time a bank pulls your credit report because you applied for something, it creates a hard enquiry on your record. One hard enquiry drops your score by approximately 5–10 points. Three applications in one month = 15–30 points gone immediately.

Worse, multiple enquiries in a short period signal financial desperation to lenders — even if you were just comparing options.

Rule: Space loan or credit card applications at least 6 months apart. Use comparison sites (PaisaBazaar, BankBazaar) to check eligibility without triggering hard enquiries — they use soft checks which do not affect your score.

Step 5 — Never Close Your Oldest Credit Card

Credit age is 15% of your score. CIBIL looks at the average age of all your credit accounts. Closing your oldest credit card reduces both your average account age and your total available credit limit — hurting your score twice.

If you have a credit card you never use, keep it open. Make one small purchase every 3 months — a ₹500 grocery bill is enough. Pay it in full immediately. The account stays active, your history grows, and your score benefits.

Step 6 — Close or Settle All Overdue and Written-Off Accounts

Overdue accounts are the heaviest negative marks on a CIBIL report. An account marked “Written Off” or “Settled” by a bank is visible on your report for 7 years and actively suppresses your score during that period.

What to do:

- Call the bank’s collections department and ask for the total outstanding amount

- Negotiate a settlement — banks often accept 50–70% of outstanding on old bad debts

- Get the settlement terms in writing before paying

- After payment, collect a No Objection Certificate (NOC) from the bank

- Ensure the bank updates CIBIL status from “Written Off” to “Closed” or “Settled”

- Verify update on your CIBIL report within 45–60 days

Important: “Settled” is still a negative mark — it means you paid less than the full amount owed. “Closed” is neutral. Always try to pay the full outstanding to get “Closed” status. Score recovery begins within 3–6 months of closure.

Step 7 — Build Credit from Zero Using a Secured Credit Card

If your score is NH (No History) or below 600 and no bank will approve you, a secured credit card is the fastest way to start building.

A secured credit card requires a fixed deposit as collateral — usually ₹10,000 to ₹25,000 minimum. The bank gives you a credit card with a limit equal to 80–90% of the FD. You use the card normally, pay on time, and the FD earns interest simultaneously.

Banks offering secured credit cards in India: SBI (SBI Advantage Plus), Axis Bank, ICICI Bank, Kotak Mahindra Bank. Apply at your existing bank where you hold a savings account — approval is near-certain since the FD covers the risk.

Use below 30% of the limit. Pay full balance every month. Within 12 months, most applicants build a score of 700+ and qualify for regular unsecured credit cards.

Step 8 — Maintain a Healthy Credit Mix

Lenders like to see that you can manage different types of credit responsibly. A person with only credit cards shows one dimension. A person with a home loan, a car loan, and a credit card — all paid on time — shows a fuller, more trustworthy picture.

You do not need to take loans just for the sake of credit mix. But if you are planning a purchase that requires a loan anyway, note that a well-managed EMI loan alongside your credit cards helps your score over time.

Step 9 — Become an Authorised User on a Family Member’s Card

If a parent, spouse, or sibling has a credit card with a long history and clean payment record, ask them to add you as an authorised user. Their positive payment history on that card appears on your CIBIL report as well — even though you are not the primary cardholder.

This is a legitimate and legal method used widely in India. It does not affect the primary cardholder’s score. The authorised user gets the benefit of inherited credit history without financial liability (the primary cardholder remains responsible for payments).

Step 10 — Monitor Your Score Monthly and Set Bill Reminders

Many people check their CIBIL score once and forget it for years. Monthly monitoring catches errors early, shows you which actions are working, and lets you dispute new incorrect entries before they cause damage.

Free monthly score checks (soft enquiries — no score impact):

- PaisaBazaar app — free, unlimited

- BankBazaar — free with detailed report

- Groww app — free instant score

- OneScore app — free with detailed breakdown

How Long Does It Actually Take to Improve CIBIL Score?

| Starting Score | Target Score | Realistic Timeline | Key Actions Required |

|---|---|---|---|

| NH / No History | 700+ | 9–12 months | Secured credit card, consistent payments |

| Below 600 | 700+ | 18–24 months | Settle overdue accounts, secured card, zero new defaults |

| 600–650 | 700+ | 9–12 months | Pay on time, reduce utilisation, no new applications |

| 650–700 | 750+ | 6–9 months | Reduce utilisation below 20%, consistent payments |

| 700–750 | 800+ | 6–12 months | Utilisation below 10%, grow credit age, dispute errors |

There is no shortcut. Any company, website, or consultant offering to “fix” your CIBIL score for a fee is running a scam. CIBIL scores cannot be changed by a third party — only your own financial behaviour over time, or legitimate error disputes, change your score.

Why Was Your Loan Rejected? — Common Reasons Beyond CIBIL Score

Sometimes your CIBIL score is 720 but a loan still gets rejected. Here is why:

| Rejection Reason | What to Do |

|---|---|

| Score below bank’s internal threshold (varies by lender) | Apply at a different bank or NBFC with lower threshold |

| Too many recent hard enquiries | Wait 6 months before applying again |

| Income too low relative to loan amount | Apply for smaller amount or add co-applicant |

| Existing EMI burden too high (FOIR above 50%) | Prepay existing loans to reduce monthly obligations |

| Employer category not accepted (some banks reject certain sectors) | Try a different bank or apply after switching jobs |

| Settled account on report (even if old) | Disclose proactively; some banks accept after 2-3 years |

| Error in report — wrong DPD (days past due) | Raise CIBIL dispute with bank NOC as proof |

Frequently Asked Questions

Q: How often does CIBIL score update?

CIBIL scores update every 30–45 days as banks report new data. Actions you take today — like paying off a balance — may not reflect on your score for 30–45 days. Patience is required.

Q: Does checking my own CIBIL score hurt it?

No. Checking your own score is a soft enquiry and has zero impact. Only hard enquiries — when a lender checks your score because you applied for credit — affect your score. Check as often as you like.

Q: Will closing a credit card hurt my score?

Yes, especially if it is an old card or one with a high limit. Closing it reduces your average account age and your total credit limit — both hurt your score. Keep cards open with minimal usage unless they have a high annual fee that is not worth it.

Q: My loan was “written off” 4 years ago. Can I still fix my score?

Yes. Pay the outstanding amount, collect the NOC, and have the bank update CIBIL to “Closed.” A written-off account stays visible for 7 years, but its negative impact reduces over time as newer positive data accumulates. Most lenders overlook a single old settled account if the last 2–3 years show clean payment history.

Q: What is a good CIBIL score for a home loan in India?

750 and above gets you the best home loan rates from SBI, HDFC, ICICI, and Axis Bank. Between 700–750 you can still get approved but may pay 0.25–0.50% higher interest — which on a ₹50 lakh loan over 20 years means paying approximately ₹3–5 lakh extra. Below 700, most major banks will reject or require a higher down payment.

Q: Can I get a loan with CIBIL score of 650?

Yes, from NBFCs and some newer banks. Bajaj Finance, Tata Capital, and digital lenders like MoneyTap or KreditBee approve loans at 650+ but at higher interest rates — typically 18–36% versus 11–15% at a bank. Use these only in genuine emergencies while working on improving your score.

Q: Is Experian score the same as CIBIL score?

No. Experian, CRIF High Mark, and Equifax are separate credit bureaus. Each has its own scoring model and score range. Experian scores in India range from 300–900 — same range as CIBIL but calculated differently. Your scores across bureaus may differ by 20–50 points. Most banks specify which bureau they use — check before applying.

Disclaimer: Educational content only. Credit scoring models, bureau policies, and bank requirements may change. Always verify current information from official CIBIL, Experian, CRIF, and Equifax websites and from respective bank websites before making financial decisions.