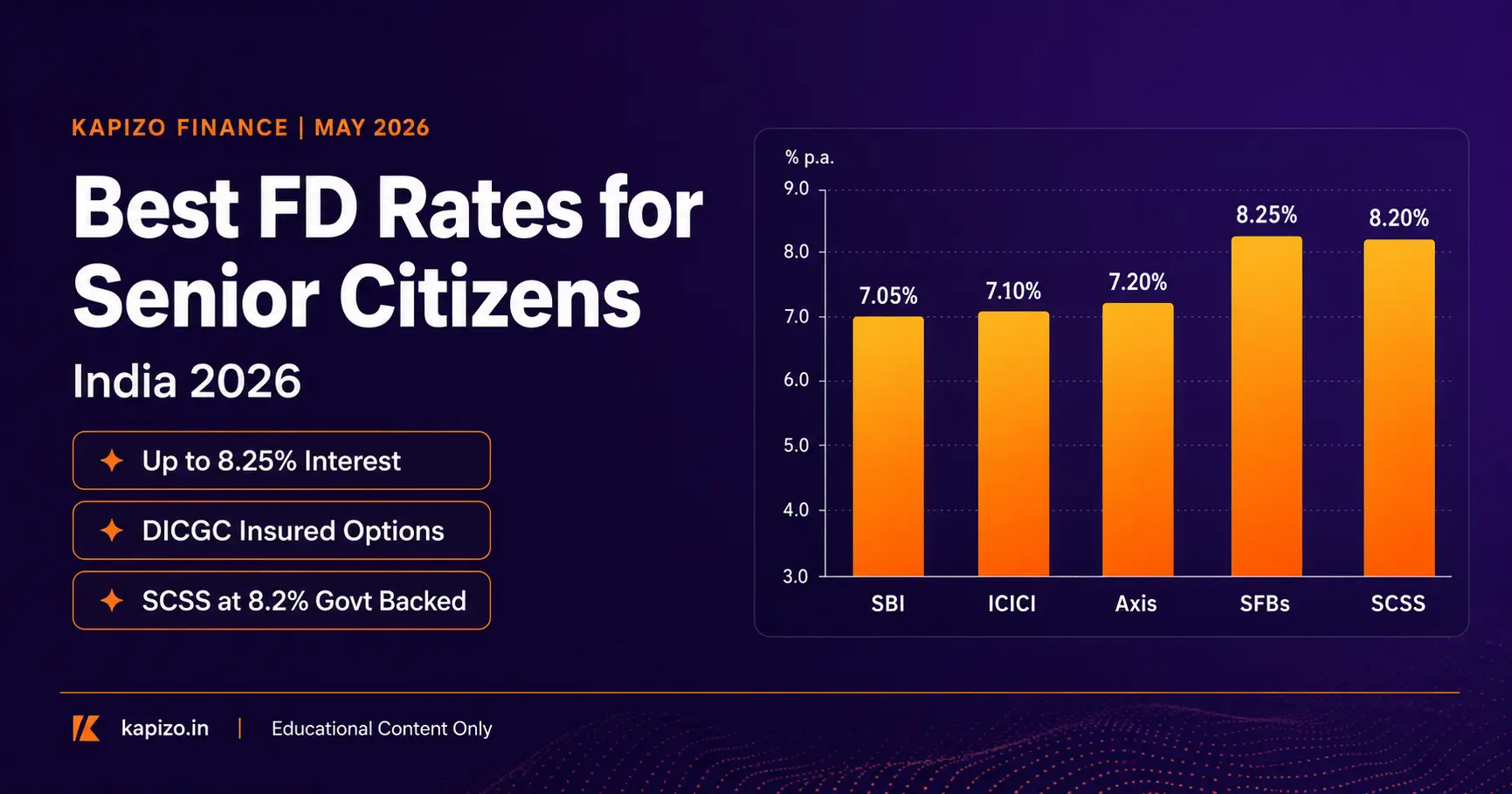

- Rate range: 6.75% to 8.25% (banks) | 8.2% SCSS (government)

- Highest bank rate: 8.25% — Suryoday SFB & Utkarsh SFB

- Safest + high rate: SCSS at 8.2% (sovereign guarantee)

- TDS threshold: ₹1,00,000/year for seniors (from April 2025)

- 80TTB deduction: ₹50,000/year (old tax regime only)

- Data verified: May 2026

Why FD Rates Matter More for Senior Citizens

Fixed deposits remain the backbone of retirement planning for millions of Indians. When a regular salary stops, the need for predictable, periodic income becomes critical- and FDs offer exactly that. But not all FD rates are equal, and senior citizens now have access to rates that are meaningfully higher than what general investors receive.

In 2026, the rate landscape has shifted considerably, with Small Finance Banks offering up to 8.25%, government schemes like SCSS at 8.2%, and even large private banks improving their senior citizen offerings. The difference between choosing the right FD and the wrong one can mean tens of thousands of rupees in additional annual income on a ₹20–30 lakh corpus.

This article is a comprehensive, data-verified guide to the best FD rates available for senior citizens (age 60 and above) in India as of May 2026. We cover public sector banks, private banks, Small Finance Banks, and government-backed schemes along with a practical tax and safety framework. For broader FD comparisons across all age groups, see our FD Interest Rates India 2026.

This is educational content only. Always verify current rates at respective official bank websites and consult a qualified financial advisor before investing.

Master Comparison Table Senior Citizen FD Rates (May 2026)

| SBI | 7.05% | 5–10 years (WeCare) | Public Bank | DICGC ₹5L | 1 May 2026 |

| Bank of Baroda | 7.00% | Above 5 yrs to 10 yrs | Public Bank | DICGC ₹5L | 5 Jan 2026 |

| Punjab National Bank | 7.10% | 444 days | Public Bank | DICGC ₹5L | 24 Feb 2026 |

| HDFC Bank | 7.00% | 3yr 1d to <4yr 7m | Private Bank | DICGC ₹5L | 6 Mar 2026 |

| ICICI Bank | 7.10% | 3yr 1d to 5 years | Private Bank | DICGC ₹5L | 5 May 2026 |

| Axis Bank | 7.20% | 5 years – 10 years | Private Bank | DICGC ₹5L | 5 May 2026 |

| IDFC FIRST Bank* | 7.50% | 450 days – 5 years | Private Bank | DICGC ₹5L | 1 Apr 2026 |

| Suryoday SFB | 8.25% | 30 months | Small Finance Bank | DICGC ₹5L | 29 Mar 2026 |

| Utkarsh SFB | 8.25% | 666 days | Small Finance Bank | DICGC ₹5L | 5 May 2026 |

| Jana SFB | 8.00% | 1 year – 3 years | Small Finance Bank | DICGC ₹5L | 11 Apr 2026 |

| Unity SFB | 8.00% | Exactly 12 months | Small Finance Bank | DICGC ₹5L | 9 Feb 2026 |

| SCSS | 8.20% | 5 years (extendable) | Govt Scheme | Sovereign Guarantee | Q1 FY2026-27 |

| Post Office TD (5yr) | 7.50% | 5 years | Govt Scheme | Sovereign Guarantee | Q1 FY2026-27 |

Public Sector Banks FD Rates for Senior Citizens

Public sector banks are the preferred choice for conservative investors who prioritise institutional safety and widespread branch networks. Their rates are generally lower than Small Finance Banks, but the trust factor, government ownership, and ease of access make them a core component of any senior citizen’s fixed-income portfolio.

State Bank of India (SBI)

SBI offers a structured set of senior citizen benefits. The flagship product is the SBI WeCare scheme, which adds an extra 50 basis points (0.50%) over the regular senior citizen rate on deposits with tenures of 5 years and above. This brings the effective best rate to 7.05% for the 5–10 year bracket, effective 1 May 2026.

SBI’s Amrit Vrishti 444-day FD offers 6.45% for senior citizens, revised down from 6.60% in December 2025. For citizens aged 80 and above, SBI’s Patrons scheme provides an additional 10 basis points (+0.10%) over the standard senior citizen rate making it a thoughtful product for the super senior demographic.

| Scheme / Tenure | Senior Rate (60–79) | Super Senior Rate (80+) |

|---|---|---|

| Amrit Vrishti (444 days) | 6.45% | 6.55% |

| 5–10 years (WeCare) | 7.05% | 7.15% |

Bank of Baroda (BoB)

Bank of Baroda’s best rate for senior citizens is 7.00% on tenures above 5 years to 10 years, effective 5 January 2026. The bob Square Drive 444-day special deposit offers 6.95% for regular senior citizens and 7.05% for super seniors (80+). BoB also provides an additional 0.10% for super seniors on tenures of above 1 year to 5 years. Notably, the senior premium on the 5–10 year tenure is +1.00% over regular rates one of the largest such premiums among public sector banks.

| Scheme / Tenure | Senior Rate (60–79) | Super Senior Rate (80+) |

|---|---|---|

| bob Square Drive (444 days) | 6.95% | 7.05% |

| Above 5 years to 10 years | 7.00% | 7.10% |

Punjab National Bank (PNB)

Punjab National Bank offers the highest rate among the three major public banks featured here. Its 444-day special tenor deposit gives senior citizens a rate of 7.10%, effective 24 February 2026. PNB stands out with the most generous super senior (80+) premium in the public bank segment: an additional +0.80% over regular rates, bringing the super senior rate on the 444-day tenure to a compelling 7.40%. For citizens aged 80 and above, PNB’s 444-day FD rivals several private bank offerings while carrying the institutional credibility of a large public sector bank.

| Tenure | Senior Rate (60–79) | Super Senior Rate (80+) |

|---|---|---|

| 444 days (special) | 7.10% | 7.40% |

Private Banks FD Rates for Senior Citizens

Private banks typically combine competitive rates with superior digital platforms, customer service, and innovative product features. Senior citizen premiums at private banks are generally a flat 0.25%–0.50% above regular rates. The four banks below represent the most relevant private bank options for senior investors in 2026.

HDFC Bank

HDFC Bank’s best rate for senior citizens is 7.00%, available on tenures from 3 years 1 day to less than 4 years 7 months, effective 6 March 2026. HDFC does not currently operate a separately branded senior citizen FD scheme the senior premium is applied as a standard addition across eligible tenures. For tax planning purposes, HDFC Bank applies the revised TDS threshold of ₹1,00,000 per year for senior citizens (applicable from 1 April 2025). This means TDS is not deducted until annual FD interest from HDFC crosses ₹1 lakh, providing useful cash flow flexibility.

ICICI Bank

ICICI Bank offers a flat senior citizen premium of +0.50% over its regular FD rates across all domestic deposits. The best rate for senior citizens is 7.10%, applicable on tenures of 3 years 1 day to 5 years, effective 5 May 2026. The ICICI Tax Saver FD also earns 7.10% for senior citizens, making it useful for those seeking both returns and a Section 80C deduction under the old tax regime.

Clarification: Some third-party sources have incorrectly referenced a “Golden Years FD” scheme from ICICI Bank. This product has not been confirmed on official ICICI Bank channels and should not be relied upon when making investment decisions.

Axis Bank

Axis Bank offers the highest FD rate among all private banks in this guide: 7.20% for senior citizens on tenures of 5 years to 10 years, effective 5 May 2026. For the 18-month to 5-year bracket, Axis provides a consistent 6.95%. This makes Axis particularly attractive for senior citizens willing to lock in funds for the medium-to-long term and seeking a step up from public bank rates without moving into Small Finance Banks.

IDFC FIRST Bank

IDFC FIRST Bank offers a best rate of 7.50% for senior citizens on tenures of 450 days to 5 years, effective 1 April 2026. Its Tax Saver FD also earns 7.50% for senior citizens. A particularly distinctive feature is zero-penalty premature withdrawal for senior citizens a rare benefit that adds meaningful liquidity to an otherwise illiquid instrument. This makes IDFC FIRST suitable for senior investors who want a higher rate but are concerned about needing access to funds before maturity.

Important note: The IDFC FIRST Bank rates and zero-penalty premature withdrawal feature cited here are sourced via Gemini AI. While these are consistent with IDFC FIRST Bank’s known positioning, please verify all current rates and product features directly at idfcfirstbank.com before making any investment decision.

Small Finance Banks Higher Rates With a Clear Framework

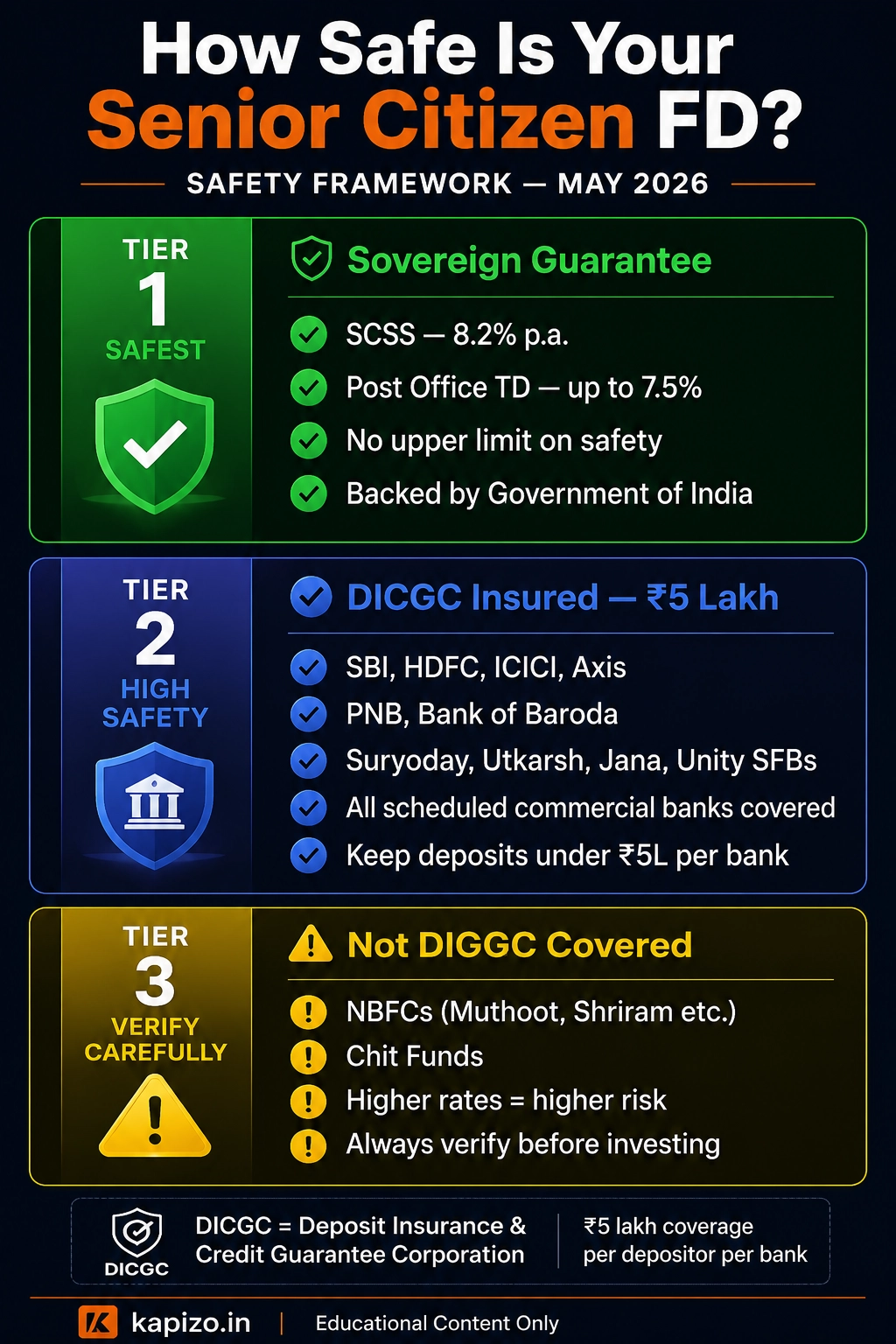

Small Finance Banks (SFBs) are RBI-licensed banking institutions specifically set up to serve underserved customer segments. They are fully regulated by the Reserve Bank of India, accept retail deposits, and are covered under the DICGC deposit insurance scheme exactly like regular commercial banks. This means deposits of up to ₹5 lakh per depositor per bank are insured against bank failure.

SFBs offer rates that are often 1.00%–1.50% higher than large public or private banks for equivalent tenures. This premium exists because SFBs compete actively for retail deposits to fund their lending operations. The trade-off is that SFBs are smaller, younger institutions. While DICGC coverage applies, prudent investors should keep total deposits per SFB including accrued interest within the ₹5 lakh insured limit. For a larger corpus, the strategy of spreading deposits across multiple SFBs is both practical and well-established.

Suryoday Small Finance Bank

Suryoday SFB offers one of the highest FD rates in India: 8.25% for senior citizens on a 30-month tenure, effective 29 March 2026. For a 5-year tenure, the rate is a strong 8.05%. The senior citizen premium at Suryoday is a relatively modest +0.15% over regular rates, but the absolute rate is among the highest available anywhere. Senior citizens comfortable with the SFB framework and DICGC insurance limits will find Suryoday’s 30-month offering highly compelling.

| Tenure | Senior Citizen Rate |

|---|---|

| 30 months | 8.25% |

| 5 years | 8.05% |

Utkarsh Small Finance Bank

Utkarsh SFB jointly holds the top position with a best rate of 8.25%, available on a very specific tenure of exactly 666 days, effective 5 May 2026. For the broader 2–3 year bracket, the rate is 8.00%. Senior citizens should note the precision involved the 8.25% rate applies only to the 666-day tenure. Booking for a slightly different duration may result in a lower rate. Confirm tenure specifics and current rates directly with Utkarsh SFB before investing.

Jana Small Finance Bank

Jana SFB offers a best rate of 8.00% for senior citizens on tenures of 1 year to 3 years, effective 11 April 2026. However, there are important nuances. Jana does not offer a senior citizen premium on tenures below 180 days. For the 3–5 year bracket, the rate drops to 7.77% the same rate offered to all age groups, meaning senior citizens receive no preferential benefit here. Jana SFB is most attractive specifically for the 1–3 year bracket where the 8.00% rate applies clearly.

Unity Small Finance Bank

Unity SFB offers 8.00% for senior citizens, but only on the exactly 12-month tenure, effective 9 February 2026. Beyond 12 months, rates drop sharply to 7.25%. This makes Unity SFB suitable specifically for senior investors who want a high short-term rate and are prepared to review and renew their FD annually. It is not the right instrument for those seeking to lock in at 8.00% for multiple years.

Across all SFBs: the higher the rate on offer, the more important it is to verify DICGC coverage, confirm exact tenure requirements, and ensure total deposits per bank remain within ₹5 lakh for full insurance protection.

Government Schemes The Safest High-Return Options

Senior Citizens Savings Scheme (SCSS)

The Senior Citizens Savings Scheme (SCSS) is a government-backed investment specifically designed for Indian residents aged 60 and above. For Q1 FY2026-27 (April–June 2026), the interest rate is 8.2% per annum, paid out quarterly. This makes SCSS the single most compelling combination of safety and return available to senior investors in India today.

SCSS carries a sovereign Government of India guarantee there is no DICGC limit, no bank counterparty risk, and no institutional failure scenario to plan for. The maximum deposit per individual is ₹30 lakh. A married couple can each hold separate accounts, allowing a combined family deposit of up to ₹60 lakh. SCSS deposits qualify for a Section 80C deduction (up to ₹1.5 lakh) under the old tax regime. The scheme runs for 5 years and can be extended for an additional 3 years at maturity.

On a risk-adjusted basis, SCSS at 8.2% with sovereign backing outperforms most bank FDs including several SFB offerings because the government guarantee eliminates credit risk entirely. For senior citizens whose primary concern is capital preservation, SCSS should be the first and largest allocation in the fixed-income portfolio. For tax planning around SCSS, see our Income Tax Guide FY 2026-27.

Post Office Time Deposits (POTD)

Post Office Time Deposits are another sovereign-guaranteed instrument available to all investors. Senior citizens do not receive a preferential rate over general investors here, but the government backing and accessibility through India’s vast post office network particularly in tier-2 and tier-3 cities make POTDs a reliable option.

| Tenure | Interest Rate (Q1 FY2026-27) | Section 80C |

|---|---|---|

| 1 year | 6.9% | No |

| 2 years | 7.0% | No |

| 3 years | 7.1% | No |

| 5 years | 7.5% | Yes |

The 5-year Post Office TD at 7.5% with 80C eligibility is a sensible complement to SCSS for investors who have already maxed out their SCSS limit or want diversification across government instruments. Rates are reviewed and announced quarterly by the Ministry of Finance.

Safety Framework Protecting Your Deposits

For senior citizens, capital safety is as important as return. Understanding deposit insurance and the risk hierarchy across different institutions is essential before committing to any FD.

What is DICGC insurance? The Deposit Insurance and Credit Guarantee Corporation (DICGC), a wholly owned subsidiary of the RBI, insures deposits up to ₹5 lakh per depositor per bank. This limit covers the combined total of all deposits held by a single depositor in the same bank savings account, current account, and all fixed deposits combined. DICGC coverage applies to all scheduled commercial banks and all RBI-licensed Small Finance Banks. If a covered bank fails, depositors are compensated up to ₹5 lakh, regardless of the total amount deposited.

Practical deposit-splitting strategy: If you have a corpus larger than ₹5 lakh, the straightforward approach is to spread deposits across multiple different banks, keeping total deposits (including projected interest) per bank below ₹5 lakh. Each bank is a separate coverage unit. For example, a ₹25 lakh corpus can be distributed across five banks at approximately ₹5 lakh each resulting in full DICGC coverage on the entire amount. This strategy is widely recommended by financial planners for senior citizens with large fixed-income portfolios.

What DICGC does NOT cover: Non-Banking Financial Companies (NBFCs), chit funds, and co-operative societies are not covered by DICGC insurance. Senior citizens should exercise particular caution with FD products offered by NBFCs, even well-known ones, as they carry credit risk without any deposit insurance safety net. Always confirm DICGC membership on the institution’s website before investing.

Government schemes are the safest tier of all. SCSS and Post Office Time Deposits are backed by the sovereign Government of India. There is no deposit limit for the government guarantee on these instruments, and they carry no institutional failure risk. For broader investment planning, including comparing FDs with market-linked instruments, refer to our SIP Investment Guide India 2026.

Tax Guide for Senior Citizens FD Interest Income

FD interest income is fully taxable in India under the head “Income from Other Sources,” and understanding the tax rules applicable to senior citizens is essential for accurate post-tax return calculations. Several important parameters changed for FY 2025-26 and FY 2026-27.

TDS threshold for senior citizens: From 1 April 2025, the TDS threshold on FD interest for senior citizens has been revised upward to ₹1,00,000 per year per bank. Banks will not deduct TDS until total FD interest earned from that bank in a financial year exceeds this limit. (For non-senior investors, the threshold remains ₹40,000.) This is a significant benefit for senior citizens with moderate FD portfolios. Importantly, not being subject to TDS does not eliminate the tax obligation the interest income is still taxable and must be declared in your Income Tax Return (ITR).

Section 80TTB deduction old regime only: Senior citizens can claim a deduction of up to ₹50,000 per year on interest income from banks, post offices, and co-operative societies under Section 80TTB. This deduction is available exclusively under the old tax regime. Investors who have opted for the new tax regime cannot claim this benefit. For those with significant FD interest income, the 80TTB deduction can meaningfully reduce tax liability, making the old regime potentially more advantageous.

Practical example: Consider a senior citizen with ₹10 lakh invested in an FD earning 7.5% annually. Annual interest income = approximately ₹75,000. Under the old tax regime: Section 80TTB allows a ₹50,000 deduction, leaving only ₹25,000 as taxable interest income, to be added to overall income and taxed at the applicable slab rate. Under the new tax regime: the full ₹75,000 is added to taxable income with no special deduction. Depending on the individual’s total income, the old regime may result in significantly lower tax.

Slab-based taxation applies regardless of TDS: FD interest is always taxed as per the investor’s applicable income tax slab, regardless of whether TDS has been deducted. Senior citizens (60–79 years) enjoy a basic exemption of ₹3 lakh under the old regime, while super senior citizens (80+) enjoy a ₹5 lakh basic exemption. For a full breakdown of tax slabs and FY 2026-27 tax planning strategies, refer to our Income Tax Guide FY 2026-27.

Which FD Is Right for You? Investor-Type Decision Framework

There is no universally “best” FD for every senior citizen. The right choice depends on your specific priorities — safety, yield, liquidity, and tax efficiency. Use this framework as a starting point for your decision-making:

- If you want maximum safety: Prioritise SCSS at 8.2% (sovereign guarantee) as your primary allocation. For amounts exceeding the ₹30 lakh SCSS limit, consider SBI or HDFC Bank for institutional comfort. SCSS offers the best combination of safety and yield available to senior citizens.

- If you want the highest absolute returns: Suryoday SFB (8.25%, 30 months) or Utkarsh SFB (8.25%, 666 days) offer the highest bank FD rates available. Keep total deposits per SFB within ₹5 lakh for full DICGC coverage. These are suitable for conservative investors who understand and accept the SFB institutional framework.

- If you want a balance of rate and institutional safety: Axis Bank at 7.20% offers the highest rate among mainstream private banks, without the additional due-diligence requirements of SFBs. IDFC FIRST Bank at 7.50% is also worth evaluating once verified directly with the bank.

- If liquidity is important: IDFC FIRST Bank’s zero-penalty premature withdrawal feature for senior citizens is a standout it allows access to funds without penalty, a meaningful benefit for investors who may need to respond to health or other emergencies. Verify this feature directly at idfcfirstbank.com.

- If you want tax-saving FDs with returns: The ICICI Bank Tax Saver FD at 7.10% or the IDFC FIRST Tax Saver FD at 7.50%* offer Section 80C benefits for old-regime investors. SCSS also qualifies for 80C and offers 8.2% making it the dominant choice for tax-saving FDs.

- If you are a super senior citizen (aged 80+): PNB’s 444-day FD at 7.40% is the standout option, leveraging PNB’s most generous super senior premium of +0.80%. Bank of Baroda’s bob Square Drive at 7.05% for super seniors is a strong BoB alternative. Both options sit within the institutional safety of large public banks. SCSS at 8.2% remains the optimal sovereign-backed option.

Frequently Asked Questions

Q1: What is the highest FD rate for senior citizens in India in 2026?

The highest FD rate for senior citizens as of May 2026 is 8.25%, jointly offered by Suryoday Small Finance Bank (30-month tenure) and Utkarsh Small Finance Bank (666-day tenure). Among government schemes, the Senior Citizens Savings Scheme (SCSS) offers 8.2% with a sovereign guarantee, making it the highest rate with absolute safety.

Q2: Is SCSS better than a bank FD for senior citizens?

For most senior citizens, SCSS offers superior risk-adjusted returns. At 8.2% with a sovereign guarantee, it beats all public banks and most private banks, with zero credit risk. Key limitations include a maximum deposit of ₹30 lakh per individual and a quarterly not monthly payout structure. For larger corpora or for those needing monthly income, a combination of SCSS and bank FDs is a practical approach. SCSS should generally be the first and largest allocation.

Q3: Are Small Finance Bank FDs safe for senior citizens?

Small Finance Banks are RBI-regulated and are covered under DICGC deposit insurance up to ₹5 lakh per depositor per bank the same protection level as large commercial banks. Deposits within this insured limit carry equivalent statutory protection. The key discipline is to keep total deposits per SFB (principal + accrued interest) below ₹5 lakh. For amounts above this, the excess is uninsured and carries institutional risk. SFBs are relatively stable, regulated entities, but have shorter operating histories than large commercial banks.

Q4: What is Section 80TTB and who can claim it?

Section 80TTB is a tax deduction available exclusively to resident senior citizens aged 60 and above. It allows a deduction of up to ₹50,000 per financial year on interest income earned from banks, post offices, and co-operative societies. This deduction is available only under the old tax regime. Senior citizens who have opted for the new tax regime cannot claim 80TTB. It is one of the most valuable tax concessions available to older investors, particularly those with FD-heavy portfolios.

Q5: What happens to FD interest under the new tax regime?

Under the new tax regime, FD interest is taxed as per your applicable income tax slab, just as under the old regime. The key difference is that the Section 80TTB deduction of ₹50,000 is not available under the new regime. This means senior citizens with substantial FD interest income could end up paying more tax under the new regime. It is advisable to compute your tax liability under both regimes before making a choice, preferably with the assistance of a qualified tax advisor or Chartered Accountant.

Q6: Can a senior citizen split FDs across banks to maximise DICGC coverage?

Yes. Splitting FD deposits across multiple banks is a straightforward and widely practised strategy to maximise DICGC insurance coverage. The ₹5 lakh limit applies per depositor per bank, so maintaining deposits of up to ₹5 lakh in each of several different banks ensures full insurance coverage on your entire FD corpus. For example, ₹25 lakh can be spread across five different banks at ₹5 lakh each, with every rupee fully insured. When calculating the ₹5 lakh limit, remember to account for accrued interest across the deposit tenure not just the original principal.

Disclaimer: Educational content only. FD interest rates, taxation rules and regulations change periodically. Verify latest rates from official bank websites and consult a qualified financial advisor before making investment decisions. Kapizo Finance is not a registered investment advisor.