Quick Summary April 2026

- Small finance banks often offer highest FD rates

- Senior citizens get 0.50% extra interest

- DICGC insurance covers Rs.5 lakh per bank

- Tax saver FD has 5-year lock-in

- FD interest taxable at income slab rate

Fixed Deposits are one of the safest investment options in India because returns are fixed and protected by bank regulations. This guide covers current FD rates April 2026, tax rules, and how to choose the right FD.

Last Updated: 29 April 2026

Sources Used

- RBI banking guidelines

- DICGC deposit insurance rules

- Income Tax Department

- Official bank FD rate pages

- April 2026 rate trackers

Public Sector Bank FD Rates April 2026

| Bank | General Rate | Senior Citizen | Best Tenure |

|---|---|---|---|

| SBI | 3.05 – 6.40% | 3.55 – 6.90% | 2-3 years |

| Bank of Baroda | 3.50 – 6.45% | 4.00 – 7.00% | Long term |

Private Bank FD Rates April 2026

| Bank | General Rate | Senior Citizen |

|---|---|---|

| ICICI Bank | 2.75 – 6.60% | 3.25 – 7.10% |

Source: Official bank websites April 2026. Rates change frequently. Verify before investing.

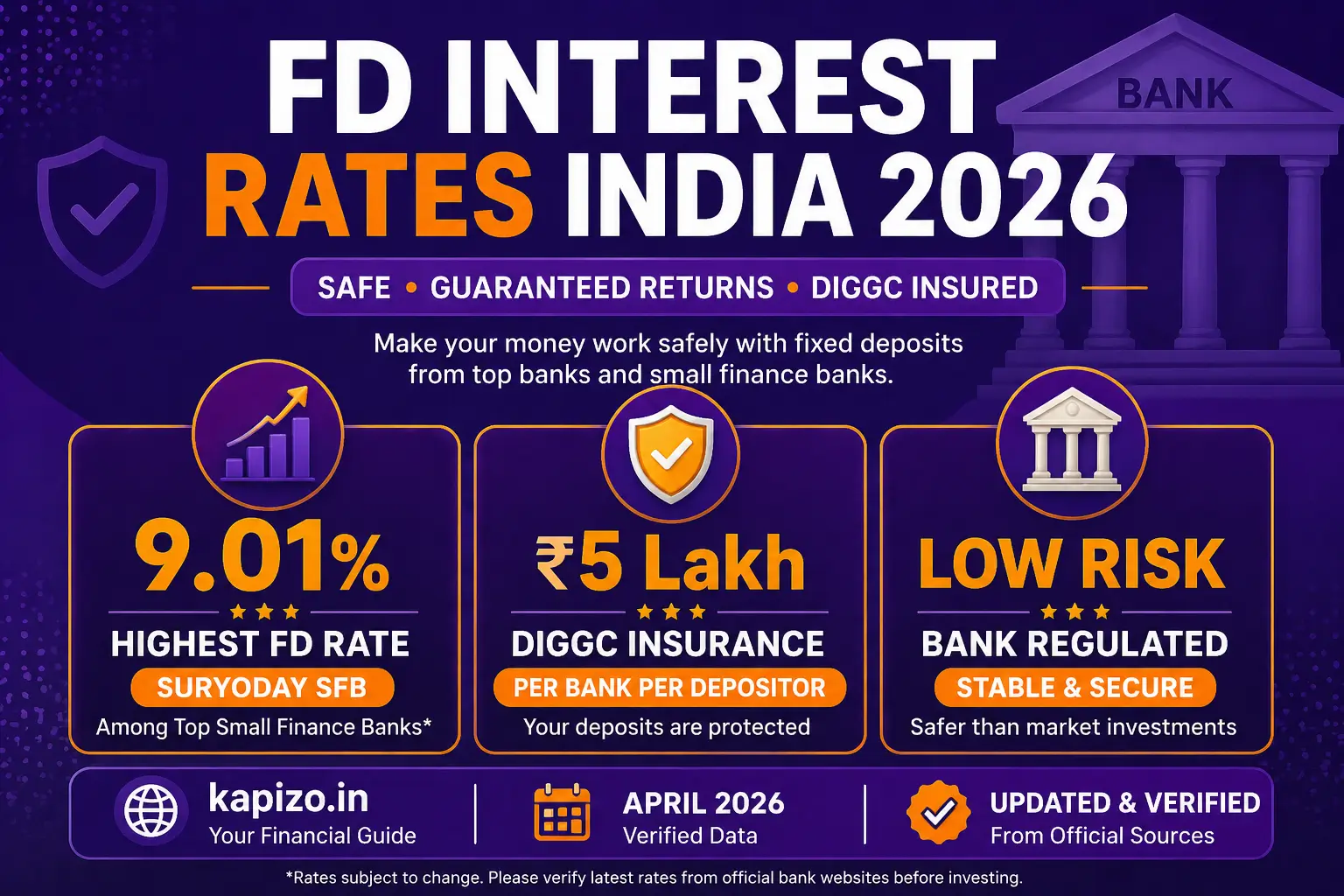

Highest Small Finance Bank FD Rates

Small finance banks often offer higher FD rates compared to large banks because they are expanding and need deposits. RBI regulates these banks. Deposits insured Rs.5 lakh per bank under DICGC.

| Bank | Rate Range |

|---|---|

| Suryoday SFB | 7.90 – 9.01% |

| Jana SFB | 7.77 – 8.50% |

| Equitas SFB | 7.00 – 8.50% |

| Ujjivan SFB | 7.20 – 8.25% |

Source: April 2026 rate trackers. Verify from official websites.

Tax Saving FD Section 80C

| Bank | Regular | Senior |

|---|---|---|

| SBI | 6.05% | 7.05% |

| BoB | 6.00 – 6.30% | 6.90 – 7.00% |

5 year lock-in. Rs.1,50,000 deduction Section 80C old regime only.

FD Tax Rules FY 2026-27

TDS Section 194A

| Category | Threshold | Rate |

|---|---|---|

| General | Rs.50,000/year | 10% with PAN |

| Senior 60+ | Rs.1,00,000/year | 10% with PAN |

| No PAN | Any amount | 20% |

FD interest added to income. Taxed at slab rate. Tax slabs may change. Verify from Income Tax Department.

Form 15G (below 60) or 15H (seniors) = avoid TDS if income below taxable limit.

Best FD Choice by Goal

| Goal | Better Option |

|---|---|

| Emergency fund | Short-term FD 1-2 years |

| Monthly income | Non-cumulative FD |

| Wealth building | Cumulative FD |

| Tax saving | 5-year FD Section 80C |

| Maximum safety | PSU bank FD |

Safest FD Banks in India

Public sector banks like SBI and Bank of Baroda are generally considered more stable by many Indian depositors because of their large size and government ownership structure.

All bank FDs insured Rs.5 lakh per bank under DICGC. Split deposits across banks for amounts above Rs.5 lakh.

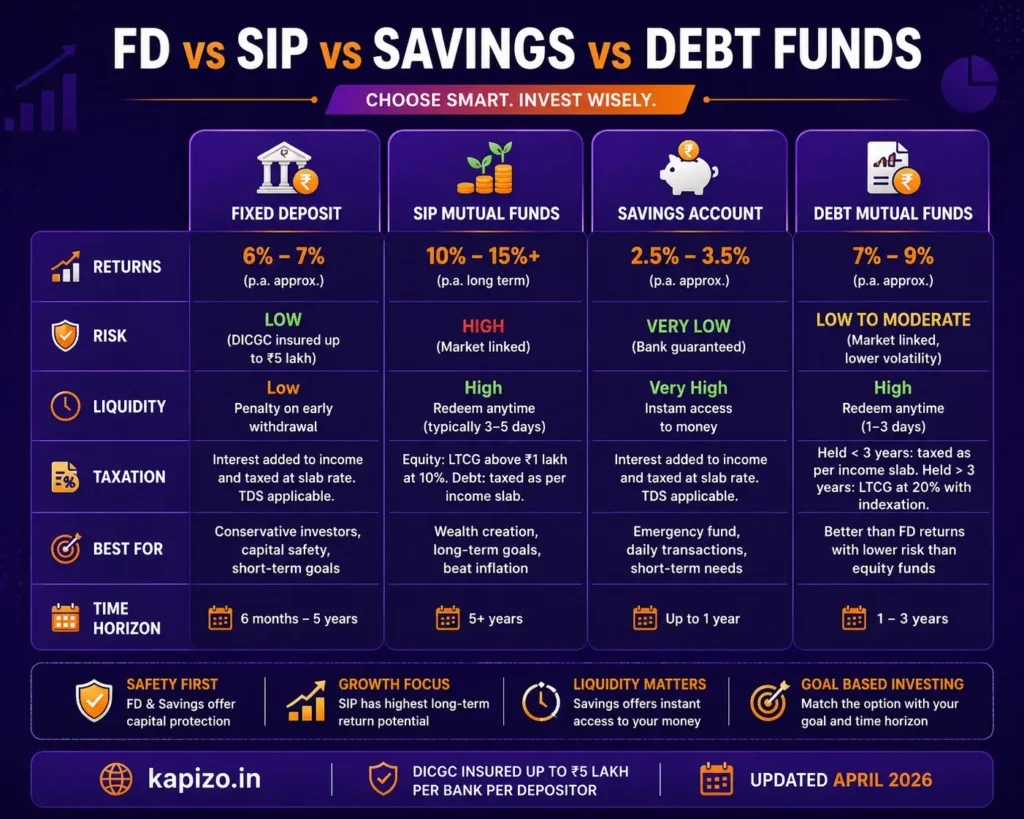

FD vs Other Options

| Option | Returns | Risk |

|---|---|---|

| Bank FD | 6-7% | Low DICGC Rs.5L |

| Small finance FD | 8-9% | Low DICGC Rs.5L |

| Post Office FD | 7-7.5% | Very low govt |

| Debt mutual fund | 7-9% | Low to moderate |

When FD is NOT a Good Option

FDs may not be ideal for long-term wealth creation because inflation and taxation can reduce real returns over time. Investors with goals beyond 5-7 years often consider equity mutual funds for potentially higher long-term growth.

Types of FDs

Regular FD = interest paid quarterly or annually

Cumulative FD = interest at maturity, better returns

Tax Saving FD = 5 year lock-in, Section 80C

Flexi FD = linked to savings account

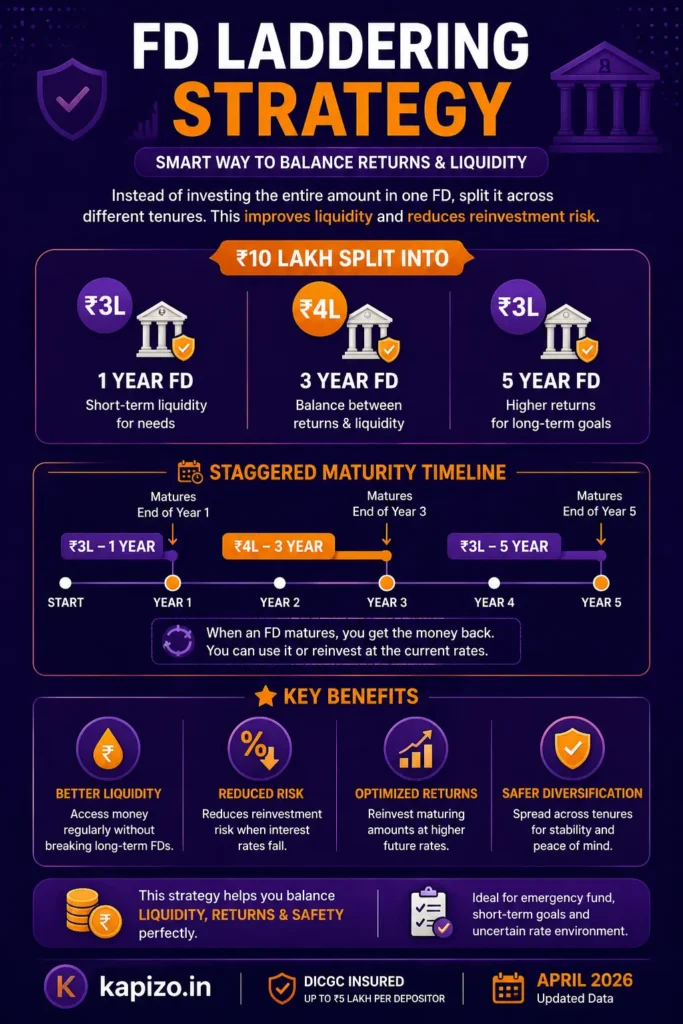

FD Laddering Strategy

Split Rs.10 lakh across maturities instead of one FD.

Rs.3L = 1 year

Rs.4L = 3 year

Rs.3L = 5 year

Improves liquidity. Reduces reinvestment risk.

Senior Citizen Extra Interest

0.50% extra at most banks for 60+.

TDS threshold Rs.1,00,000 vs Rs.50,000 for general.

DICGC Insurance

Rs.5 lakh per bank per depositor.

Example: Rs.9L in SBI = only Rs.5L covered.

Solution: SBI Rs.5L + HDFC Rs.5L + ICICI Rs.5L = Rs.15L fully insured.

Premature Withdrawal

Penalty 0.50 – 1.00%.

Tax saving FD = no withdrawal before 5 years.

Common Mistakes

Investing above Rs.5L in single bank

Not submitting Form 15G or 15H

Choosing regular over cumulative

Breaking FD early

Not comparing rates

Ignoring small finance banks

How to Choose

Compare 3-4 banks

Check DICGC limit

Match tenure to goal

Submit Form 15G or 15H if eligible

Choose cumulative for compounding

Related Financial Guides

- SIP Investment Guide India 2026

- Personal Loan Guide India

- Income Tax Guide FY 2026-27

- Home Loan Guide India 2026

Frequently Asked Questions

Q: What is best FD rate India April 2026?

Suryoday Small Finance Bank was among higher FD rate providers in April 2026. ICICI offers 7.10% for seniors. Verify from official bank websites.

Q: How is FD interest taxed?

Added to income. Taxed at slab rate. Banks deduct 10% TDS above thresholds.

Q: Is small finance bank FD safe?

Yes. DICGC-covered (up to Rs.5 lakh) Rs.5 lakh per bank. Do not exceed Rs.5 lakh in single bank.

Q: Can I break FD early?

Yes, penalty 0.50 – 1.00%. Tax saver FD has 5 year lock-in, no early exit.

Q: What is DICGC limit?

Rs.5 lakh per bank per depositor. Split across banks if investing more.

Disclaimer: FD rates, tax rules and bank policies may change periodically. Verify latest information from official bank websites and Income Tax Department before investing. Educational content only. Not investment advice. Kapizo.in may earn affiliate commission.