What is FD Laddering? Strategy, Examples, and Benefits for Indian Investors

Updated: 18 May 2026

Many Indian families make one common FD mistake.

They lock all their savings into:

- one bank

- one FD

- one tenure

At first, this feels simple.

But later, problems appear:

- emergency cash becomes inaccessible

- premature withdrawal penalties reduce returns

- better interest-rate opportunities are missed

- liquidity becomes tight during unexpected expenses

This is where FD Laddering becomes useful.

FD laddering is a practical strategy that helps investors balance:

- returns

- liquidity

- flexibility

- financial safety

Instead of putting all money into one long-term FD, the amount is split across multiple fixed deposits with different maturity periods.

This creates periodic access to cash while still allowing part of the money to remain invested for longer durations.

For conservative Indian investors, retirees, salaried families, and emergency fund planners, FD laddering can become a more flexible alternative to locking everything into one deposit.

Disclaimer: FD rates, bank policies, taxation, and premature withdrawal rules may change. Verify latest details from official bank websites before investing. Educational content only.

What Is FD Laddering?

FD laddering is a strategy where money is divided into multiple fixed deposits with different maturity dates.

Instead of:

- investing ₹5 lakh into one 5-year FD

the amount is split into smaller deposits.

Example:

| FD | Amount | Tenure |

|---|---|---|

| FD 1 | ₹1 lakh | 1 Year |

| FD 2 | ₹1 lakh | 2 Years |

| FD 3 | ₹1 lakh | 3 Years |

| FD 4 | ₹1 lakh | 4 Years |

| FD 5 | ₹1 lakh | 5 Years |

This structure creates:

- yearly maturity access

- periodic liquidity

- reinvestment flexibility

- reduced dependence on one interest-rate cycle

Why Locking All Money Into One FD Can Become a Problem

Many investors focus only on:

- highest FD rate

- longest tenure

But real-life financial situations change unexpectedly.

Suppose someone locks:

₹5 lakh into one 5-year FD.

Problems may appear if:

- medical expenses arise

- job loss happens

- interest rates increase later

- emergency liquidity becomes necessary

Breaking an FD early often reduces returns through:

- penalty charges

- lower applicable interest rates

That is why liquidity matters.

FD laddering helps reduce this problem by ensuring part of the money matures periodically.

How FD Laddering Works

The process is simple.

Step 1 — Divide the Investment

Split the total amount into equal or planned portions.

Step 2 — Choose Different FD Tenures

Use staggered maturity periods such as:

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

Step 3 — Reinvest Matured FDs

When the shortest FD matures, the amount can be:

- used for expenses

- reinvested into a new long-term FD

- shifted based on market conditions

Over time, this creates a rolling ladder structure.

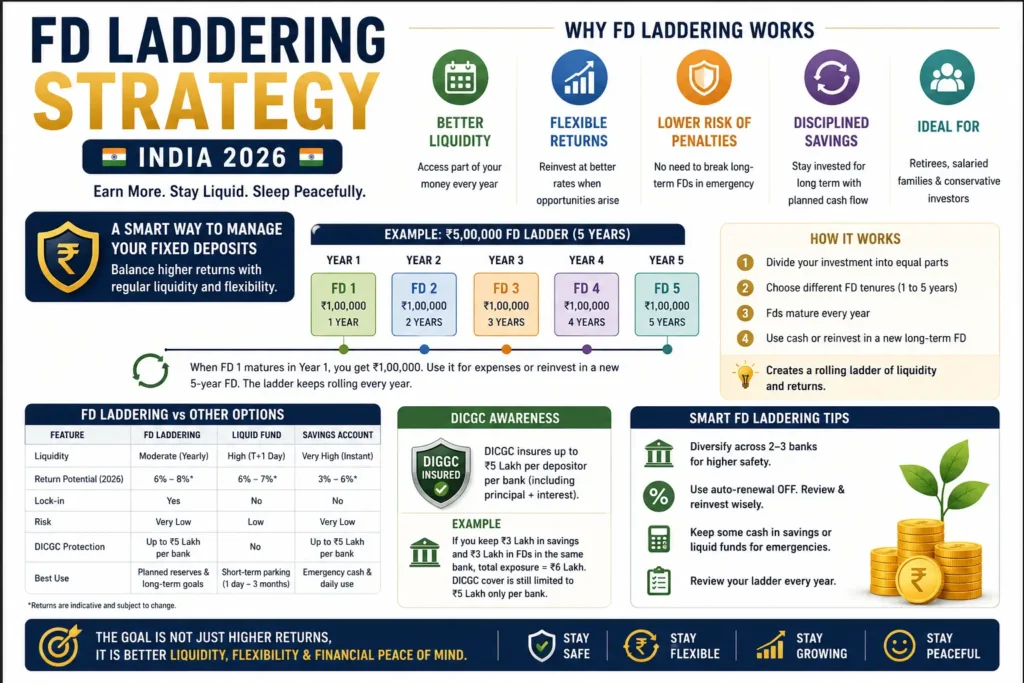

Example: ₹5 Lakh FD Ladder Strategy

Here is a practical example for Indian households.

| FD | Amount | Maturity |

|---|---|---|

| FD 1 | ₹1 lakh | 1 Year |

| FD 2 | ₹1 lakh | 2 Years |

| FD 3 | ₹1 lakh | 3 Years |

| FD 4 | ₹1 lakh | 4 Years |

| FD 5 | ₹1 lakh | 5 Years |

After Year 1:

- FD 1 matures

- investor gets liquidity access

- amount can be reinvested into another 5-year FD

This process continues yearly.

The investor avoids locking the entire corpus for one long duration.

Main Benefits of FD Laddering

1. Better Liquidity

This is the biggest advantage.

Instead of waiting years for access to money, part of the portfolio matures periodically.

Useful for:

- retirees

- emergency reserves

- salaried families

- conservative investors

2. Lower Premature Withdrawal Risk

Breaking a long FD early usually reduces returns.

Many banks apply:

- lower interest rates

- premature withdrawal penalties

FD laddering reduces the chances of breaking the full investment.

3. Better Interest Rate Flexibility

Interest rates change constantly.

If all money is locked during a low-rate cycle, investors may miss better future opportunities.

With laddering:

- some money matures regularly

- reinvestment can happen at newer rates

4. Reduces Reinvestment Pressure

Instead of deciding what to do with the full corpus at once, investors review smaller portions periodically.

This improves financial flexibility.

FD Laddering vs Single Long-Term FD

| Feature | FD Laddering | Single Long FD |

|---|---|---|

| Liquidity | Higher | Lower |

| Flexibility | Better | Limited |

| Emergency Access | Easier | Difficult |

| Reinvestment Opportunity | Periodic | Delayed |

| Simplicity | Moderate | Very Simple |

| Interest Rate Risk | Spread Out | Concentrated |

Who Should Use FD Laddering?

FD laddering may suit:

- senior citizens

- retirees

- salaried employees

- conservative investors

- emergency fund planners

- families needing periodic liquidity

It is especially useful for investors who:

- dislike market volatility

- prefer stable planning

- want predictable cash flow

Who May Not Need FD Laddering?

Some investors may prefer simpler structures.

Examples:

- short-term parking below 6 months

- very small FD amounts

- highly active investors using debt funds

- investors comfortable with market-linked products

FD Laddering and Emergency Funds

One major advantage of laddering is liquidity planning.

Many Indian households mistakenly lock emergency money into long-tenure FDs.

That creates problems during:

- medical emergencies

- sudden travel

- job loss

- urgent repairs

A better structure may look like:

| Purpose | Suggested Option |

|---|---|

| Instant emergency cash | Savings account |

| Short-term reserve | Liquid fund |

| Medium-term reserve | Short FD |

| Long-term reserve | FD ladder |

This creates better financial flexibility.

FD Laddering vs Liquid Funds vs Savings Accounts

| Feature | FD Ladder | Liquid Fund | Savings Account |

|---|---|---|---|

| Liquidity | Moderate | High | Very High |

| Return Potential | Moderate | Moderate | Lower |

| Lock-in | Yes | No | No |

| Stability | High | Moderate | High |

| DICGC Protection | Yes | No | Yes |

| Best Use | Planned reserves | Short-term parking | Instant cash access |

One important difference:

FDs lock in rates for the chosen tenure.

Liquid funds adjust gradually with changing market conditions.

That is why many investors combine:

- savings accounts

- liquid funds

- FD ladders

instead of depending on only one option.

Important DICGC Rule Investors Should Know

DICGC insurance applies:

per depositor per bank

Many investors misunderstand this.

If a person keeps:

- ₹3 lakh in savings

- ₹3 lakh in FDs

inside the same bank,

total exposure becomes:

₹6 lakh

But DICGC insurance still applies only up to:

₹5 lakh per depositor per bank

This includes:

- principal

- accumulated interest

combined.

That is one reason diversification across banks can matter for large deposits.

Common FD Laddering Mistakes

1. Locking All FDs in One Bank

Diversification matters for large deposits.

2. Ignoring Emergency Liquidity

Not all money should remain locked.

3. Chasing Only Highest Rates

Higher rates should not override:

- liquidity

- diversification

- safety planning

4. Forgetting Tax Impact

FD interest remains taxable according to applicable tax slabs.

Practical FD Laddering Strategy for Indian Families

A balanced structure may look like:

- emergency cash in savings account

- short-term reserve in liquid fund

- medium and long-term reserves in FD ladder

- diversification across 2–3 banks

This improves:

- stability

- liquidity

- flexibility

- emergency preparedness

FAQs

What is FD laddering?

FD laddering is a strategy where money is divided into multiple fixed deposits with different maturity dates.

Is FD laddering better than one long FD?

For many investors, laddering provides better liquidity and flexibility compared to locking all money into one FD.

Is FD laddering safe?

FD laddering itself is a planning strategy. Safety depends on:

- bank selection

- diversification

- liquidity planning

Can senior citizens use FD laddering?

Yes. Many retirees use laddering for periodic maturity access and income planning.

Does FD laddering improve returns?

Its main goal is balancing liquidity and flexibility, though it may also improve reinvestment opportunities over time.

Can I break one FD in a ladder?

Yes. One advantage is that investors may only need to break a smaller FD instead of the full corpus.

Is FD laddering useful during changing interest rates?

Yes. Regular maturity cycles allow investors to reinvest gradually at newer rates.

Conclusion

FD laddering is not about chasing the highest return.

It is about:

- better cash flow management

- flexibility

- liquidity planning

- reducing financial stress

For many Indian families, locking all savings into one FD creates unnecessary pressure during emergencies or changing interest-rate cycles.

A structured ladder approach helps balance:

- stability

- access to money

- reinvestment flexibility

without depending entirely on one maturity date.

In personal finance, liquidity matters as much as returns.

Suggested Internal Links

- Are Small Finance Bank FDs Safe in India?

- SIP During Market Fall in India

- Emergency Fund Guide

- Senior Citizen FD Strategy

- Low-Risk Investment Options India

Suggested CTA

Download:

“FD Ladder Planning Checklist for Indian Families”

Includes:

- FD maturity planner

- emergency liquidity worksheet

- diversification tracker

- reinvestment review template